Key Takeaways

-

Arguments about who could tax, what could be taxed, and how far governments could reach are as old as the country itself.

- Federalism produces thousands of overlapping tax jurisdictions, reflecting local priorities but creating real complexity for taxpayers.

- Expect the next 250 years to bring broader nexus standards, more taxation of services and the digital economy, and continued competition between states.

In 1776, the American experiment officially began, but its origins trace back even further, to a familiar dispute over taxes. Long before 1040s and compliance calendars, arguments about who could tax, what could be taxed, and how far governments could reach helped spark a revolution. Two hundred and fifty years later, those questions remain at the heart of state and local tax policy. Who ever said taxes are boring?

Nothing Is More American Than Arguing About Taxes

At the start of it all, Americans objected to paying taxes to a government that did not represent them. It was important that the government collected and used their money in a way that reflected their voices and needs.

In the early years of the country, government systems were relatively weak, and taxes mostly took the form of local property taxes and simple levies. But over time this changed. In the 1800s, the economy was primarily agrarian, with most wealth tied up in land, livestock, and tangible goods, the kinds of assets you could easily identify and value. The easiest and perhaps “fairest” ways to impose taxes were through either a property tax or an excise tax on specific goods or transactions. These taxes were also easy to administer because they did not require a complicated system of tracking income. Consequently, property taxes and excise taxes were the primary way that states and local governments raised revenue until the 1930s.

And as is common throughout history, a catastrophe was a catalyst for change. The Great Depression caused property values to fall precipitously. At the same time, state governments found themselves in need of greater revenue to support relief efforts. A decade later, World War II drove another surge in spending. Old tax systems couldn’t keep pace.

In response, income and sales taxes expanded significantly. Income taxes flexed with earnings, while sales taxes were broader and more stable.

While the 16th Amendment to the U.S. Constitution, ratified in 1913, granted Congress the authority to tax income directly, the concept had existed at the state level since the mid-1800s. Many early state income taxes were temporary, very limited, or poorly enforced. In 1911, Wisconsin became the first state to implement an income tax system that resembles the modern model, although it initially only applied to the highest earners.

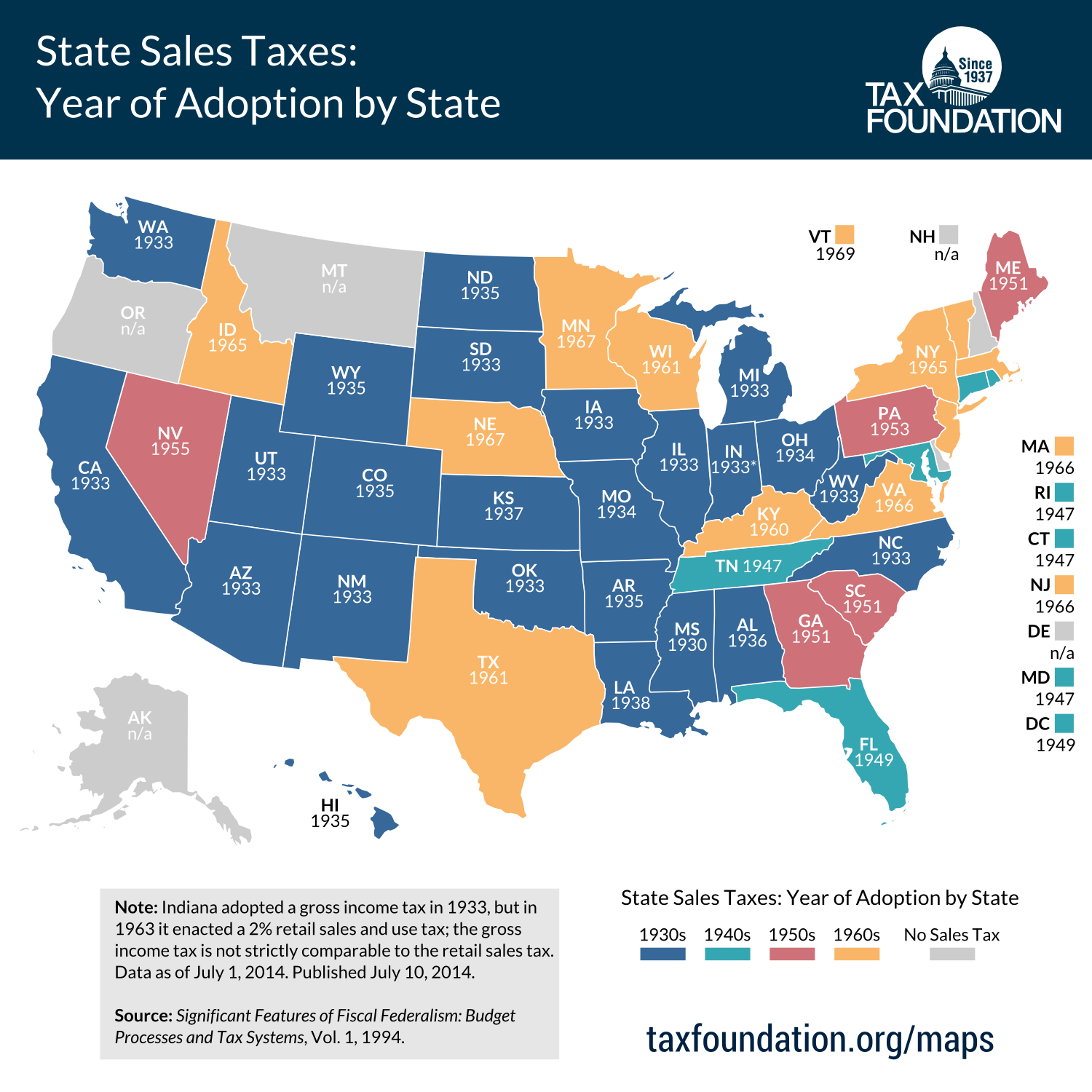

Mississippi adopted the first general sales tax in 1930, and 21 other states adopted it within the next decade. Today, only five states do not have a statewide sales tax (though Alaska allows local sales taxes).

Today’s arguments about market-based sourcing, economic nexus, and millionaires’ taxes may sound very different from colonial protests over tea and stamps, but they ultimately ask the same questions: who should pay, and which government gets to collect as the economy changes?

Those arguments are uniquely complicated in the United States because taxing authority is spread across multiple levels of government. The result isn’t one system, but thousands of overlapping tax jurisdictions, each reaching its own conclusions about what to tax and how.

What Makes SALT Uniquely American: One Country, Thousands of Tax Jurisdictions

We have all heard that the U.S. Constitution established a federalist system. But what does that mean? Simply put, it means that multiple levels of government share authority over the same territory. States, counties, cities, school districts, and special districts all play a role, leading to different rules and different outcomes depending on where you live or do business. In many ways, these differences are a feature, not a flaw, of the American system. Just as colonists wanted a greater voice in how taxes were imposed, states and local governments continue to shape tax policy based on the priorities of their own residents and communities. The result is a tax landscape that reflects local control, even when it makes life harder for taxpayers.

For example, New York exempts certain clothing from state sales tax, but local jurisdictions may continue to tax these items if they have not adopted the same exemption. Sometimes local jurisdictions will impose tax on something surprising that reflects their local values, such as Philadelphia’s sugar-sweetened beverages tax or Chicago’s recently enacted social media amusement tax.

Chicago Rolls Out Social Media Amusement Tax, Sales Tax Institute

These differences illustrate one of the enduring tensions in state and local tax policy. Communities often want flexibility to raise revenue and pursue local priorities, but businesses and taxpayers generally prefer consistency and simplicity.

Fortunately, many states simplify compliance by administering local taxes centrally, so taxpayers file one return and make one payment for all local sales taxes for the period. The exception here is Colorado, which famously (at least among tax nerds) has 108 home rule cities, approximately 68 of which administer their own sales tax systems.

What Will We Be Arguing About Next?

Who knows what the next 250 years will bring? Current trends point towards expanding business incentives, broader nexus standards, and continued efforts to tax services and the digital economy.

As the economy evolves, tax systems will likely follow, whether that means taxing more services, experimenting with new frameworks, or increasing competition between states. But if the past 250 years are any guide, one thing is certain: we’ll still be arguing about who pays, what gets taxed, and how far governments can reach.