Key Takeaways

-

Sales tax nexus is triggered by physical presence or economic activity, with economic nexus typically measured against a $100,000 sales threshold.

- States are steadily trending away from the 200-transaction threshold

- Which sales count towards the sales threshold varies by state and requires careful analysis

Sales tax economic nexus has changed more in the past decade than in the prior fifty years. What was historically rooted in physical presence has evolved into an economic standard that now affects virtually every business engaged in interstate commerce. Understanding the origin of economic nexus, the framework established after South Dakota v. Wayfair, Inc., and the ongoing trend toward simplification—particularly the elimination of transaction thresholds—is critical for taxpayers navigating today’s compliance landscape.

Historical Background: From Physical Presence to Economic Presence

2018, the guiding standard for state sales tax nexus was established by two U.S. Supreme Court decisions: National Bellas Hess v. Department of Revenue (1967) and Quill Corp. v. North Dakota (1992). These cases held that, under the Commerce Clause, a business must have a “physical presence” in a state—such as property, employees, or offices—before the state could require it to collect and remit sales tax.

While administratively straightforward, the physical presence rule became increasingly outdated with the rise of e-commerce. States faced mounting revenue losses as remote sellers grew their market share without a corresponding sales tax obligation. In response, states began enacting economic nexus provisions in anticipation of a legal challenge to the Quill standard.

That challenge came in South Dakota v. Wayfair, Inc., decided on June 21, 2018. The Supreme Court overturned Quill and held that physical presence is no longer required. Instead, states can now impose sales tax collection obligations based on a taxpayer’s “economic and virtual contacts” with the state, as long as the rules do not unduly burden interstate commerce.

The Wayfair Framework and State Adoption

The Court in Wayfair upheld South Dakota’s economic nexus law as constitutional, highlighting several key features that reduced the risk of undue burden. These included: a clearly defined threshold ($100,000 in sales or 200 separate transactions), prospective application, and participation in the Streamlined Sales and Use Tax Agreement (SSUTA), which standardizes certain compliance requirements.

Following the decision, nearly every state with a sales tax adopted its own economic nexus standard, generally modeled after South Dakota’s law. While there is some variation, most states initially implemented a threshold of $100,000 in gross sales into the state, 200 separate transactions, or both.

This uniformity provided a degree of predictability; however, the nuances within each state’s statute or guidance quickly created complexity, particularly in defining what constitutes “sales” for purposes of threshold determination.

Components of Economic Nexus: What Counts Toward the Threshold?

Although often simplified as a dollar or transaction threshold, the calculation of economic nexus is not always straightforward.

Most states measure gross sales or gross receipts sourced to the state, but the details vary. In many jurisdictions, gross sales includes all revenue from sales of tangible personal property, digital goods, and services delivered into the state, regardless of taxability. This means both taxable and exempt sales are generally included in the threshold calculation, unless the statute explicitly provides otherwise.

Some states make a distinction between taxable sales and total sales, counting only those transactions that would be subject to tax absent an exemption. This approach is less common but can significantly impact whether a taxpayer meets the threshold, particularly for businesses with a high volume of exempt sales (e.g., resale transactions or sales to exempt entities).

Additionally, states differ in their treatment of types of income:

- Marketplace-facilitated sales. Some states exclude them from the seller's threshold; others require inclusion even though the marketplace handles collection.

- Services. Treatment depends on whether the state taxes services broadly or only specific categories.

- Sales for resale. Some states include them in the threshold; others don't.

Given these differences, taxpayers must carefully review each state’s statutes and administrative guidance to ensure an audit-defensible determination of nexus exposure.

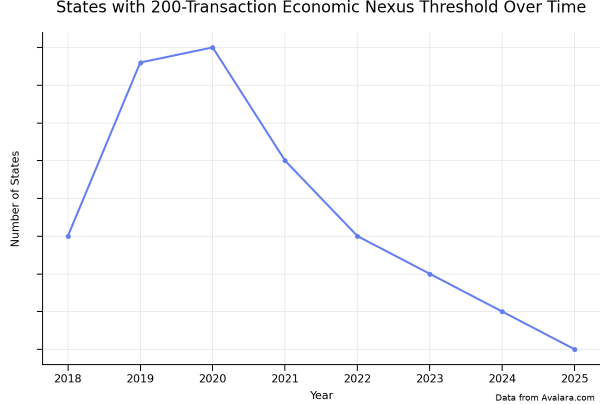

The 200-Transaction Threshold: Intent and Practical Challenges

When initially adopted, the 200-transaction threshold was intended to capture remote sellers with a significant number of low-dollar transactions that might not meet the $100,000 revenue threshold.

However, in practice, the transaction threshold created disproportionate compliance burdens for small and mid-sized sellers. A business selling low-cost items could exceed 200 transactions in a state with relatively minimal revenue, triggering full sales tax registration, collection, and filing obligations. This outcome raised concerns about administrative efficiency and fairness, particularly for businesses with limited back-office infrastructure.

From a compliance perspective, tracking the number of annual transactions by state also proved more complex than tracking gross receipts. This added an additional layer of operational burden, especially for companies operating across multiple platforms or sales channels.

Emerging Trend: States Eliminating Transaction Thresholds

In response to these concerns, a clear trend has emerged: states are increasingly eliminating the 200-transaction threshold and relying solely on a sales-based standard, typically $100,000 in gross sales.

Over the past several years, 16 states including California, Illinois, and Washington, have amended their laws or administrative guidance to remove the transaction count requirement. Kentucky joins the list effective August 1, 2026. This shift reflects a broader policy objective to simplify compliance, reduce administrative burden, and focus enforcement on businesses with more meaningful economic presence in the state.

The move toward a single, receipts-based threshold also enhances consistency and audit defensibility. Gross sales are generally easier to track, reconcile, and substantiate through accounting records, whereas transaction counts may vary depending on system configurations, order bundling, and definitions of a “separate transaction.”

Notably, while the trend is widespread, it is not yet universal. Approximately 15 states, Puerto Rico, and Washington D.C. continue to maintain a transaction threshold, requiring taxpayers to monitor both criteria. As a result, a comprehensive nexus analysis must still account for each jurisdiction’s specific requirements.

Practical Implications for Taxpayers

The evolution of economic nexus has fundamentally shifted the compliance landscape. Businesses cannot rely solely on physical presence to determine their sales tax obligations; instead, they must proactively monitor their economic activity in each state.

From a practical standpoint, this means:

- Tracing state-by-state revenue (and transaction counts where they still matter)

- Knowing what each state includes in "sales", including the treatment of exempt transactions and marketplace activity.

- Reviewing the business footprint for changes in nexus at least annually, or more frequently if experiencing rapid growth

Conclusion

Economic nexus represents one of the most significant developments in state and local tax in recent history. What began as a response to the limitations of the physical presence standard has evolved into a complex but increasingly standardized framework for remote sellers.

The shift away from transaction thresholds simplifies one part of the analysis, but the harder questions about what counts as a "sale" in each state remain complex.

For taxpayers, that means carefully monitoring economic activity and applying each state's rules correctly. Sellers who don't put in the work face the consequences later, often in the form of audit assessments, penalties and interest.