Empower your team with AI and automation solutions built for growth. Unlock your full potential.

Get insight at the speed of now with accurate, reliable data.

Who We Are

Eide Bailly is a CPA firm bringing practical expertise in tax, audit, and advisory to help you perform, protect, and prosper with confidence.

Key Takeaways

- Data integrity is the foundation for successful AI adoption.

- Clean, well-governed data unlocks automation and advanced analytics.

- AI is not one-size-fits-all. Assess your business processes to identify strategic applications for AI.

AI adoption is accelerating — but execution is lagging. Gartner predicts that 60% of AI projects will be abandoned due to a lack of AI-ready data, while more than 40% of agentic AI initiatives are likely to be canceled by 2027 as organizations struggle to translate hype into business value. CEOs and IT leaders rank AI as a top priority, yet many organizations struggle with fragmented systems, poor data hygiene, and unclear objectives.

To harness AI’s full potential, you need a strategic approach to data — one that aligns technology, people, and processes for measurable impact. Poor data quality, inadequate security, and governance issues can hamper the most ambitious AI strategies.

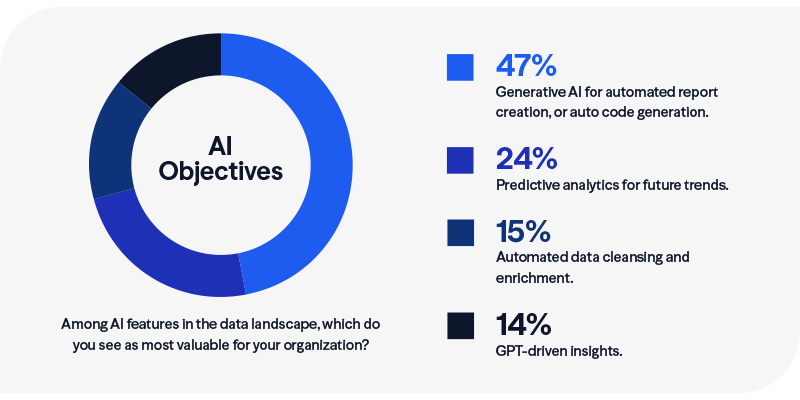

Set Your AI Goals

It’s important to have a clear understanding of what you hope to gain from AI before any work can be done.

To begin, assess your processes. Identify where AI can create the most impact, whether it’s automating repetitive tasks, uncovering insights from customer data, or improving forecasting.

5 Steps to Optimize Your Data for AI

Once you’ve identified your AI objectives, it’s time to look at your data. In our recent survey, only 6% of business leaders reported having data that is well-structured and secure.

Here’s how to optimize your data:

- Accumulate Raw Data

Gather historical and real-time data from across your organization—transactional systems, customer interactions, and connected devices. The more relevant data you collect, the smarter your AI will become. -

Practice Good Data Hygiene

Cleanse your data by fixing errors, removing duplicates, and resolving inconsistencies. Reliable data prevents AI from making inaccurate or biased decisions. -

Unify Your Data

Break down silos by consolidating information into a centralized warehouse. A single source of truth ensures your AI has full access to the data it needs to perform effectively. -

Govern Your Data

Implement regular quality checks, enforce privacy standards, and control access to sensitive information. Effective governance ensures your data is accurate, secure, and compliant. - Annotate and Organize

Add clear, descriptive labels to your data assets so AI can learn effectively. Use plain language that reflects each asset’s content, purpose, and attributes.

Leveraging AI-Enhanced Integrations and Automations

- Integrate Systems

Use AI to automate the detection of anomalies in financial data, streamline workflows, and enable seamless data flow between platforms. Well-organized data allows AI to pull information from the right places, draw conclusions, and execute correctly. - Automate Manual Processes

Automation removes repetitive work, freeing teams to focus on strategic, high-impact tasks. This boosts operational output and job satisfaction. - Focus on Security and Compliance

In regulated industries, pay meticulous attention to data security, integration, and compliance. Vet data-handling processes and implement stringent security measures.

Maximizing ROI on IT Spend

AI is not one-size-fits-all. Assess your business processes to identify strategic applications for AI, such as generative AI for content creation or machine learning for predictive analytics.

Next, invest in training so your employees can use AI effectively and ethically. This includes establishing a governance framework with guidelines around costs, roles, compliance, and decision-making.

IT and finance teams should work together to ensure technology investments drive both innovation and financial stability.

Here are a few examples of strong data-driven AI in action:

- Cybersecurity: AI can respond faster to a variety of cyberattacks and potential threats by constantly scanning data as it comes in. Use it to scan your emails and web traffic. If AI identifies an anomaly, it can identify and triage the potential threat with specific if-then actions.

- Financial Data Analysis: Specific indicators often signal potential issues or anomalies within financial data. By integrating AI, you can automate the detection of these red flags in your financials, significantly accelerating the anomaly detection process.

- Customer Support: AI-powered chatbots and virtual assistants can be integrated into the workflows of automation solutions to handle routine customer inquiries, providing instant support and freeing up human agents for more complex tasks.

- Predictive Maintenance: Businesses that rely on machinery and equipment can use AI to analyze sensor data and predict when maintenance will be needed. Automation tools can then automate the scheduling of maintenance tasks, ensuring that issues are addressed before they lead to downtime.

Real-World Impact: Driving Quoting Efficiency with Agentic AI

One company’s sales team faced challenges with manual quoting — time-consuming processes, error-prone data entry, and reliance on external spreadsheets. To overcome these inefficiencies, we implemented a tailored Salesforce solution that simplifies and accelerates quoting workflows.

How We Helped:

- Built an integrated solution using Agentforce, Data Cloud, Flows, and custom development

- Automated opportunity and quoting workflows

- Reduced quoting time and manual errors through intelligent prompts and contextual automation

- Surfaced dynamic product and pricing information during quote creation

- Enhanced Salesforce adoption and user satisfaction with guided interactions

- Leveraged Data Cloud insights to support high-volume quoting at scale

Organizations that prioritize data quality, integration, and governance see measurable improvements in efficiency, forecasting, and customer experience. By consolidating data, automating processes, and investing in upskilling, you lay the groundwork for scalable, secure, and impactful AI.

We Can Help You Take the Next Step in AI

Eide Bailly helps organizations harness AI responsibly, aligning technology with strategy, data integrity, and human oversight.

- Take the AI Readiness Assessment

Frequently Asked Questions:

How do I know if my business is ready for AI?

Your business is ready for AI when your data is accurate, accessible, unified, and well-governed. AI depends on high-quality data to deliver reliable insights. If your organization has clearly defined goals, clean and organized data, and established governance around privacy and security, you’re better positioned to implement AI effectively.

What’s the ROI timeline for AI adoption?

AI ROI varies by use case, but organizations typically see value when they align AI investments with high-impact, measurable business problems. Automations can yield returns quickly by reducing manual work, while machine learning and predictive analytics often require more time due to data preparation.

Is AI secure for sensitive data?

AI can be secure — if your data governance, access controls, and security measures are mature. Successful AI adoption requires strict oversight of how data is collected, shared, and used. For regulated industries, this includes compliance with sector-specific standards and documented processes for privacy protection, risk management, and monitoring.

How does AI impact workforce productivity?

AI increases productivity by automating repetitive tasks, improving decision-making with real-time analytics, and enhancing workflows across departments.

What industries benefit most from AI?

Industries with rich data and operational complexity gain the greatest value. These include manufacturing, healthcare, construction, financial services, and more.