Key Takeaways

-

In this four‑part series, we lay out the playbook for state and local tax credits and incentives—and why they’ve become such a powerful tool for businesses.

- Part IV brings those concepts together through a real‑world case study, illustrating how the same project can produce very different incentive outcomes depending on location.

- Complete the State Credits & Incentives Request for Assessment if you have a project you'd like to discuss with Matt Carlson.

Throughout this series, we’ve explored what state and local tax credits and incentives are (Part I), which industries benefit most (Part II), and how the process works from planning through compliance (Part III). In this final installment, we bring those concepts together through a real world case study— showing how incentives work in practice and why outcomes can vary significantly by state.

State and Local Tax Credits and Incentives Case Study

To illustrate how SALT credits and incentives work in practice, consider the following manufacturing expansion project evaluating three potential locations.

The Project at a Glance

- Industry: Manufacturing

- Locations Considered: Minnesota, Iowa, and Colorado

- Capital Investment:

- Building purchase: $4.5 million

- Leasehold improvements: $500,000

- Manufacturing equipment: $350,000

- Furniture and fixtures: $150,000

- Workforce Impact:

- 30 net new employees over three years

- Average wage of $60,000

- Ongoing training costs of $500,000 per year

How the Same Project Produces Different Incentive Outcomes

When this project is evaluated across Minnesota, Iowa, and Colorado, the underlying facts remain the same: identical capital investment, hiring plans, and operational needs. What changes—and materially impacts the outcome—is how each state structures and prioritizes its incentive programs.

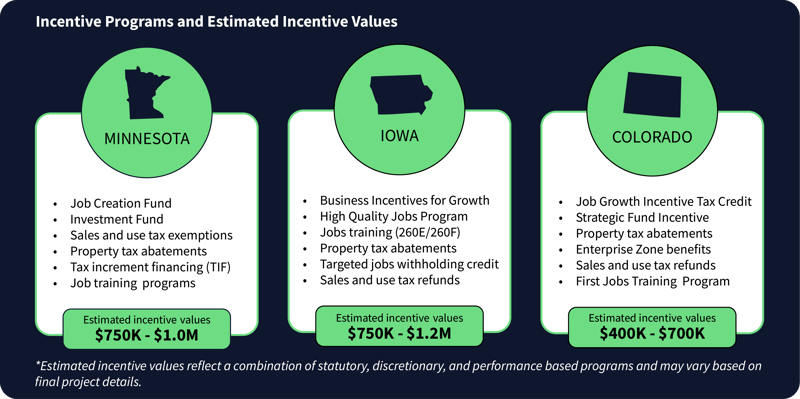

MINNESOTA

Minnesota rewards projects that strike a balance between capital investment, job creation, and workforce development. The state places meaningful emphasis on facility investment and equipment purchases, while also supporting long term employment through training focused programs. For this project, incentives tied to real estate investment, sales and use tax exemptions, property tax relief, and job training combine to produce a solid and predictable outcome. Minnesota’s estimated incentive value falls in the $750,000 to $1 million range, driven by the project’s capital intensive profile and sustained workforce investment.

IOWA

Iowa, by contrast, places greater weight on job quality and program layering. While capital investment still matters, Iowa’s incentive structure is designed to reward projects that meet wage thresholds, invest heavily in training, and create long term employment. The availability of multiple performance based and refundable programs allows incentives to stack over time, increasing total value as the project ramps up. As a result, Iowa delivers the highest potential incentive range, estimated between $750,000 and $1.25 million, despite the project being identical to the one evaluated in Minnesota.

COLORADO

Colorado’s outcome reflects a more selective and discretionary approach. While the state offers job growth credits, grants, property tax abatements, and training support, many programs are competitive or targeted to specific regions and policy goals. Incentive value tends to scale more significantly with higher job counts, higher wages, or enterprise zone eligibility. For this project, that structure results in a more modest incentive range of approximately $400,000 to $700,000, even though capital investment and hiring levels are similar to the other states.

Why This Matters

Incentives rarely change what a company does—but they often influence where and how a project moves forward. Understanding state specific priorities early can materially shift total project cost and improve overall economics.

Bottom line: Incentives don’t reward projects equally—states reward different behaviors.

Key Takeaways from the Case Study

- The same project can produce significantly different incentive results depending on location.

- Large capital investments often drive more incentive value than wages alone.

- Training programs materially impact incentive outcomes in certain states.

- Incentives are not automatic—early modeling and timing matter.

- Understanding both statutory and discretionary programs is critical when comparing locations.

This case study highlights why SALT credits and incentives should be evaluated early—before a location decision is finalized. When modeled correctly, incentives can materially change project economics and influence where and how a business grows. The key is knowing what’s available, where opportunities diverge, and how to align project facts with state and local priorities.

SALT Credits & Incentives: Frequently Asked Questions (FAQs)

Are SALT credits and incentives only for large companies?

No. While large, headline grabbing projects often receive attention, many incentive programs are available to mid market and growing businesses. In fact, smaller projects can sometimes benefit more proportionally, depending on location, industry, and timing.

Are credits and incentives guaranteed?

No. Most programs require an application, negotiation, and approval process. Incentives are often discretionary and subject to performance requirements, such as meeting investment or hiring thresholds.

What types of incentives are most common?

Common incentives include investment tax credits, job creation credits, sales and use tax exemptions, property tax abatements, training grants, and forgivable or low interest loans. The mix depends heavily on the state and project type.

Do wages matter more than capital investment?

Not always. While wages are important, many programs place greater weight on upfront capital investment—such as land, buildings, and equipment—especially during the negotiation phase. A capital intensive project can often generate more value than a labor heavy project with higher wages.

Are incentives still available for remote or office based businesses?

Yes, but availability can be more limited. Office projects may qualify for incentives tied to job creation, urban redevelopment, or targeted industries, but they typically generate smaller packages than manufacturing or infrastructure heavy projects.

When should incentives be evaluated during a project?

As early as possible. Many programs require applications to be submitted—and approved—before a project is publicly announced or construction begins. Waiting too long can reduce or eliminate eligibility altogether.

What does the incentives process typically look like?

The process generally includes project modeling, site comparison, application and negotiation, approval, implementation, and ongoing compliance. Each step requires coordination between tax, legal, finance, and operational teams.

Are incentives a one time benefit?

Often no. Many incentives are earned over multiple years and require ongoing compliance reporting. Failing to meet job or investment commitments can result in clawbacks or reduced benefits.

Why can the same project generate different incentive results across states?

Each state prioritizes different policy goals and uses different incentive structures. Factors such as capital weighting, job thresholds, training support, and local participation can dramatically change the outcome.

Does the “best” incentive package always mean the best location?

Not necessarily. Incentives should be evaluated alongside workforce availability, operating costs, infrastructure, and long term business strategy. Incentives can tip the scales—but they should not be the sole deciding factor.

For businesses considering a new build, expansion, relocation, or hiring initiative, identifying available state and local incentives early can make a meaningful financial difference—and help avoid missed opportunities or costly missteps. If you’re ready to explore what may be available for your project, complete our State Credits & Incentives Request for Assessment. The form takes approximately five minutes, and Matt Carlson will follow up to discuss potential opportunities tailored to your specific plans.