Key Takeaways

- Administration moves cannabis to Schedule III, and out of Sec. 280E.

- Sec. 280E prevents deduction of ordinary business expenses.

- Many transition questions remain for state-legal weed businesses.

- IRS moves to fire lead investigator of Malta, Puerto Rico shelters.

- Key Treasury tax figure linked to Malta deals.

- Bessent defends IRS enforcement cuts.

- National Cherry Cheesecake Day.

Trump administration reclassifies state-licensed medical marijuana as less dangerous drug - Sarah Davis, The Hill:

The order shifts the designation of licensed medical marijuana from a high level of regulation to a much looser level. It also provides a tax break to licensed medical marijuana operators

...

Blanche said Thursday in a post on social platform X that the order calls for an “expedited hearing” to reschedule marijuana and state-licensed marijuana, approved by the Food and Drug Administration (FDA), from Schedule I to Schedule III.

From Blanche's post on X:

• Immediately rescheduling FDA-approved marijuana and state-licensed marijuana from Schedule I to Schedule IIl

• Ordering a new, expedited hearing with set deadlines, to fully reschedule marijuana

This is a huge deal for the tax lives of state-legal cannabis sellers. The move from Schedule I to Schedule III takes state-legal weed out of Sec. 280E, which prohibits deductions for anything other than direct inventory costs for Schedule I and II drug businesses.

In other words, state-legal weed businesses will be taxable on net income, like other businesses, rather than gross income. They will be able to deduct normal business expenses like salaries, rents, taxes, and depreciation.

The IRS will need to provide transition guidance, starting with the effective date. Will these expenses be deductible only starting today? Next year? Or will they be deductible for the entire current taxable year? Also: do these businesses get a clean slate for choosing accounting methods, including the application of inventory capitalization rules?

UPDATE: The order apparently distinguishes between "medical" and recreational cannabis. This means purely recreational weed dealers apparently remain subject to Sec. 280E. This give the IRS one more problem, distinguishing "dispensaries" from "recreational" outlets.

Banking is also a problem for these businesses because cannabis remains illegal under federal law. Current banking regulations make it difficult for cannabis businesses to do normal banking, requiring the use of cash, cryptocurrency, or other awkward workarounds to pay taxes and expenses. Until that changes, legal weed commerce will continue to pose unique challenges.

Related: Eide Bailly Accounting Methods Services.

IRS Prepares to Fire Agent in Case Involving Key IRS Official

IRS Seeks to Fire Lead Agent in Malta, Puerto Rico Probes - Lauren Loricchio and Sarah Paez, Tax Notes ($):

...

“I was told by a current IRS-CI executive that his government whistleblowing was p------ everyone off and that he would be gone by summer,” said a tax attorney who previously worked for the government, speaking on the condition of anonymity.

The Malta pension strategy made the IRS Dirty Dozen list of "scams and schemes." A key IRS official was involved. From the Tax Notes article:

Before Kies joined the second Trump administration, his firm Federal Policy Group LLC was engaged by a company, Water Structures LLC, that offered Malta pension plans. Kies strategized with advisers about how to resist IRS efforts to curb abuse of the structures.

The implications of this for enforcement against the Malta plans and in general remain to be seen.

The IRS Funding Battle

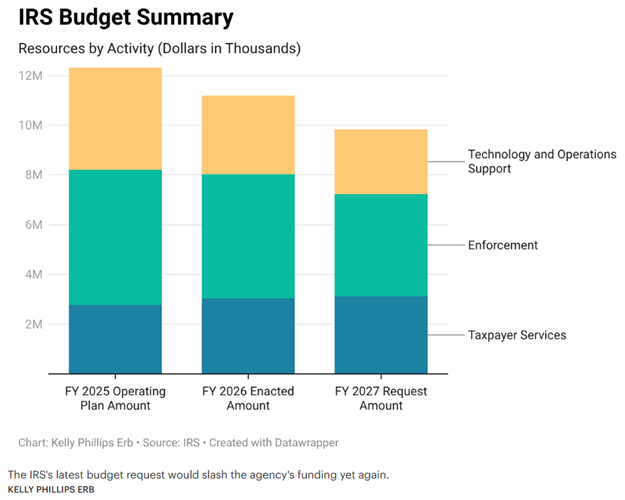

Bessent Defends Proposed IRS Budget Cuts, Focus on Tech Projects - Cady Stanton, Tax Notes ($):

Bessent called what would amount to a 12.5 percent budget reduction a “modest decrease” and argued that a focus on technology upgrades has allowed the IRS to see greater productivity, higher satisfaction among taxpayers, and lower costs.

The president’s budget, released April 3, requests for the agency $3.1 billion for taxpayer services, $4.1 billion for enforcement, and $2.6 billion for technology and operations support. Those amounts equate to a minor cut for taxpayer services, a $900 million cut for enforcement, and a $600 million cut for technology and operations support compared with fiscal 2026.

House Appropriations Committee Advances Bill to Cut IRS Funding - Tyrah Burris, Tax Notes ($):

The committee passed the fiscal 2027 bill on a 34-28 vote April 22 after debating for two days over cuts to funding for IRS staffing and enforcement.

The bill, which will now go to the House floor, would give the agency its smallest budget in two decades and its lowest enforcement funding since fiscal 2000.

IRS Enforcement Takes Another Big Hit As Budget Request Shrinks - Kelly Phillips Erb, Forbes: "The IRS saw a 27% reduction in total staffing between January and December 2025, falling from about 102,000 to 74,000 employees. The latest IRS budget proposal would eliminate another 4,000 positions, bringing IRS staffing to its lowest level in the modern era."

Court Strengthens IRS "Substance" Enforcement Tool

Liberty Global Seen Boosting IRS on Economic Substance Doctrine - Michael Rapoport and David Schultz, Bloomberg ($):

The Tenth Circuit Court of Appeals sided with the IRS’s application of the “economic substance doctrine”—the idea that a company’s transactions must have a legitimate business purpose to qualify for tax benefits—in disallowing deductions that Liberty Global had claimed.

As a result, the IRS “will likely be more aggressive in using economic substance doctrine,” said Tyler Martinez, director of litigation for the National Taxpayers Union, a taxpayer-advocacy group that filed a brief supporting Liberty Global.

Related: Eide Bailly IRS Dispute Resolution and Collections Services.

Tariff Refunds: The Theft Threat, the Trump Memory Threat.

Tariff refunds will total billions of dollars. Fraudsters are ready. - Linda Miller, Washington Post:

The importer’s controller clicks through and updates the account information. Weeks later, the refund arrives — just not to them.

...

The most immediate vulnerability is not fabricated claims — it is interception. Modern fraud inserts itself into legitimate workflows: compromising an importer’s log-in credentials, spoofing a broker’s email, or inducing a controller to update banking details through a convincing phishing page. The underlying claim can be valid, and CBP will process it as designed. The money simply goes to the wrong place.

Trump says he will 'remember' companies that don't seek tariff refunds - David Lawnder, MSN:

...

"If they don't do that, I'll remember them. I will tell you that, because I'm looking to make this country strong," the Republican president said.

Trump, who has characterized the payment of tariffs by U.S. importers as a patriotic act, on Tuesday appeared to characterize American companies that are pursuing refunds as the "enemy."

It's an unusual approach, threatening companies trying to recover illegally paid taxes for their shareholders. It doesn't jibe with the administration's approach to other tax refunds. Meanwhile, the President seeks $10 billion from the IRS as damages for his leaked returns, which is more than most refunds.

Related: Eide Bailly Transfer Pricing Services.

International Taxes: Labor Taxes in Europe; Work Needed on Global Minimum Tax

Tax Burden on Labor in Europe, 2026 - Alex Mengden and Michael Christl, Tax Foundation Europe:

Individual income taxes, payroll taxes, and consumption taxes make up a large portion of many countries’ tax revenue. These taxes combined make up the tax burden on labor, both by taxing wages directly and by taxing wages used for consumption. This so-called tax burden on labor reflects the difference between an employer’s total cost of an employee and the employee’s net disposable income.

Payroll taxes are typically flat-rate taxes levied on wages, in addition to the taxes on income. In most European countries, both the employer and the employee pay payroll taxes. These taxes usually fund specific social programs, such as unemployment insurance, health insurance, and old-age insurance. Although payroll taxes are typically split between workers and their employers, economists generally agree that both sides of the payroll tax ultimately fall on workers.

The comparable U.S. labor tax burden is around 30 percent.

Tax News & Views International Weekly: OECD's Extra Work - Alex Parker, Eide Bailly:

But, that doesn’t mean work on the tax, also known as Pillar Two, is finished. The agreement will require several more design tweaks which the OECD has yet to fully flesh out, including safe harbors to try to make it workable. And, in addition, there were several previously announced Pillar Two-related projects which had been put on the backburner while the side-by-side agreement was being negotiated.

Blogs and Bits

What tax records to keep and for how long - Kay Bell, Don't Mess With Taxes. "There’s no federal tax law or Internal Revenue Service regulation detailing a preferred way to keep your tax records. That’s because every taxpayer situation is different."

Eric Swalwell Claims Raise Tax Issues For Swalwell & His Victims - Robert Wood, Forbes. "Most people believe that sexual assault and abuse legal settlements in particular should not be taxed by the IRS. Yet how lawsuit settlements are taxed is nuanced, the tax law has long been unclear, and many sexual harassment plaintiffs have a hard time getting tax-free treatment."

Tax Day Reality Check: No Real Tax Cuts, Just $4.2 Trillion in New Debt and More Bureaucracy - Alan Dlugash, Tax Politix:

IRS Secret Shopper Strikes Again

Cleveland income tax preparer charged with filing false returns - IRS (Defendant name omitted, emphasis added):

According to court documents, she learned to prepare returns while working at a national tax return preparation company from about June 2016 to April 2017. Thereafter, she started her own tax return preparation business under different entity names, as well as her own name.

During the investigation, agents discovered that when Defendant prepared tax returns for clients, she allegedly attached fraudulent Schedule C documents (used to indicate business profit and losses) to clients’ Form 1040—even though the clients did not own businesses. Defendant also employed other schemes to avoid tax due and owing to the IRS by her clients.

Court documents say the IRS used an undercover agent - a secret shopper - in their investigation. The IRS also likes to use secret shoppers when a business is up for sale. The shopper typically asks for the tax returns to document the income, and all too often the seller volunteers that the tax returns don't show the "real" income - with disastrous consequences. Stay clean, don't cheat, and be careful out there.

What day is it?

It's National Cherry Cheesecake Day! The cherries make it low-cal.