Key Takeaways

- IRS tips as we enter the final few weeks of the filing season.

- How IRS personnel problems will lead to snags for flawed filings.

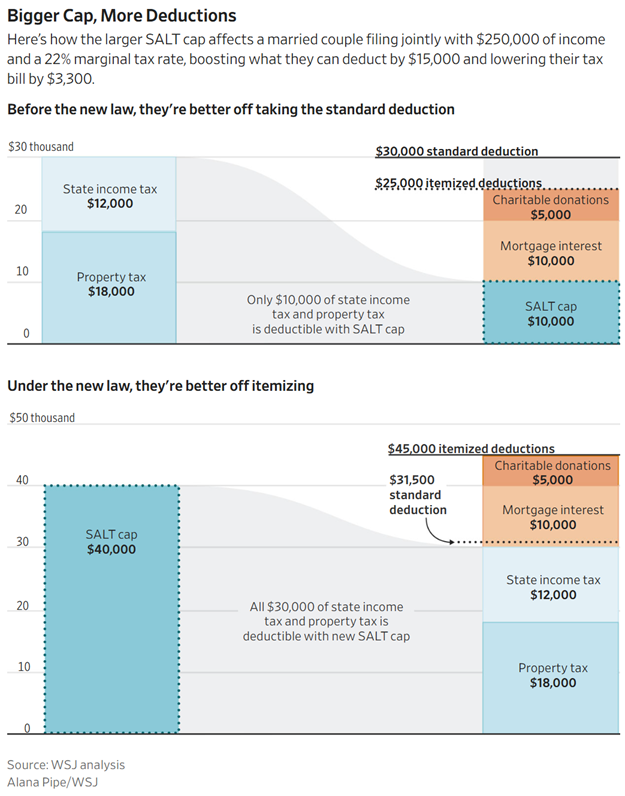

- Higher salt cap helps out blue-state filers.

- The tax dark cloud to athlete NIL windfalls.

- Another reconciliation bill?

- The puzzling tariff refund process.

- How your website might make you a state tax target.

- National Pencil Day.

Tax Time Guide: Steps taxpayers can take now to resolve tax issues and stay on track - IRS:

This Tax Time Guide focuses on what to do now.

Step 1: Prepare to file your return

Before filing, taxpayers should review their return to ensure all income is reported and deductions are claimed correctly, including any deductions reported on Schedule 1-A.

Taxpayers should keep records that support the amounts on their returns, such as pay statements or other documentation.

Step 2: Review your return before filing

Taxpayers who have not yet filed required returns should file as soon as possible, even if they cannot pay the full amount they owe. Filing allows taxpayers to:

-Claim available deductions and credits

-Reduce failure-to-file penalties

- Access payment and resolution options

Electronic filing remains the fastest and most accurate way to submit a return. The IRS encourages taxpayers to file electronically to ensure timely delivery of their returns.

Another reason to e-file is that taxpayers don’t need to be concerned about whether their return is timely postmarked. A paper tax return is treated as filed on the date it is postmarked. The Postal Service reaffirmed through a recent announcement that the postmark might be later than the date that an item is dropped in a mailbox. Taxpayers who file a paper return on the deadline, however, can request a manual postmark at post offices during business hours.

Step 3: Make a payment, even if it is partial

Taxpayers who owe taxes are encouraged to pay as much as they can by the deadline. Paying even part of the balance can reduce penalties and interest. Electronic payment options are available through IRS.gov.

I would add: If you aren't sure your return is correct, or if you are missing information, extend. That gives you six months to get your information together and file a correct return. It's always better to extend than to file and amend.

How IRS is Holding Up

Backlogs, Job Holes Plague IRS in Tax Season After DOGE Cuts - Erin Schilling and Erin Slowey, Bloomberg ($):

But in the year since DOGE’s creation, its biggest impact at the IRS—reducing its workforce—has resulted in delays in tax season preparations and data security concerns, according to agency insiders and industry observers.

Trump’s promise to modernize the IRS hasn’t materialized. Instead, according to current and former employees, the agency is largely repackaging existing initiatives and remains in the early stages of new technology as millions of Americans are filing their taxes.

This story is largely sourced from discussions with officials of the Treasury employee union, who were happy to talk to reporters. IRS officials declined to talk with the reporters, who had to piece together the IRS side from other sources, including podcast transcripts.

The story is consistent with what we are seeing. Returns with no errors that are e-filed with banking information and electronic payments of taxes due are processed smoothly. Anything else faces often-long delays as the promised automation lags behind the personnel cuts.

The Blue State Trump Dividend

Blue-State Residents Are Reaping Big Refunds From Trump Tax Law’s SALT Cap - Richard Rubin and Ashlea Ebeling, Wall Street Journal:

Millions of taxpayers—largely those who earn between $150,000 and $600,000—are starting to reap the benefits of a change that lets them deduct far more of their state and local taxes, or SALT, from their federal taxable income. In last year’s tax law, Congress raised the cap for that deduction to $40,000 from $10,000.

That means people with high state income taxes and local property taxes can pay less to the federal government, and those people are concentrated in such states as New York, New Jersey and California.

.

Taxes Always Make the Final Four

March Madness, NIL, and (Tax) Brackets - Erin Collins, NTA Blog:

Without clear guidance, it is easy to fall behind or face unexpected taxes.

...

NIL income can create layered tax issues, especially when athletes receive compensation from multiple sources with different reporting requirements. Tax complexity related to NIL income can escalate quickly, particularly for young taxpayers who may have little experience with the tax system. Without guidance, these young taxpayers may face unexpected tax bills, penalties, or compliance challenges.

In many cases, student-athletes receive NIL income without any taxes withheld, and they may be surprised to learn they owe taxes when they file their returns. Non-cash compensation such as trading cards, apparel, use of a vehicle, and unlimited food vouchers must generally be included in income at its fair market value, which can be difficult to determine. Student-athletes may suddenly find themselves responsible for estimated tax payments, deciding whether to form a business entity, and figuring out how federal, state, and local tax rules apply. In addition, they may need to determine whether self-employment tax applies and which expenses, if any, are deductible.

Don't count on an IRS turnover to enable you to shoot a winning three at the buzzer. They control the clock.

Tax Policy: Second Reconciliation?

Capitol Hill Recap: Second Tax Go-Around - Alex Parker, Eide Bailly:

But events have conspired to change that calculus. Republicans and the Trump Administration have been looking to appropriate funds towards the military action in Iran, as well as Immigration and Customs Enforcement. The Republican leadership has begun to look to reconciliation as a way forward, forgoing the usual appropriations process.

That would provide a vehicle to pass other items that couldn’t make the cut for OBBBA, or which have otherwise failed to move forward in Congress so far. It’s bound to include tax-related items, as reconciliation can only contain measures that have a budgetary effect.

It’s still early, and this is far from a sure thing. But while 2026 looked to be a relatively quiet year in Congress, it’s turning out to be anything but.

Meanwhile in Tariff-land

IEEPA Tariff Refund Process - Chad Martin, Eide Bailly:

CBP provided a target go-live for CAPE of 45 days, suggesting refunds could begin as early as late April. It also laid out a four-step process for importers to claim refunds under CAPE:

1. Importers or their customs brokers must submit a CAPE Declaration via the new web-based portal in the Automated Commercial Environment (ACE). This involves uploading CSV files with a list of entry summaries for the IEEPA refunds.

2. CAPE will automatically remove the tariff codes from each entry and recalculate the total duties owed as if those tariffs never applied.

3. CAPE schedules a date to finalize (liquidate or reliquidate) the entries and applies interest (currently at 6% for corporations) to the final amount owed.

4. Refunds are consolidated by the Importer of Record (IOR) and paid electronically.

...

Importers who have paid IEEPA tariffs are advised to closely follow developments in these cases and make sure they have supplied CBP with up-to-date information.

Tussling for Tariff Refunds - Lee Sheppard, Tax Notes ($)

But the administration wants to drag it out.

Is it possible to simplify the procedure for smaller importers? Lizbeth R. Levinson of Fox Rothschild has filed 100 claims at the CIT on behalf of large and small importers. For unliquidated entries, a CIT complaint should be filed. For liquidated entries for which the 180 day protest period has not expired, the importer must file a protest with CBP. Levinson advises filing both a CIT complaint and a protest — a preemptive belt-and-suspenders approach. More than 2,500 plaintiffs have filed complaints at the CIT. “Any importer that takes these two actions will be well protected,” Levinson says.

How the Internet Can Make You Taxable in a State

SALT Digital Nexus and Sourcing Risks: Key State Tax Developments to Watch - Melissa Menter and Colette Sutton, Eide Bailly:

Digital advertising remains a prime revenue target—but not without resistance. As more states look to tax digital ad services directly or indirectly, taxpayers are increasingly challenging whether these regimes run afoul of the Internet Tax Freedom Act. Litigation over Chicago's novel social media tax and Minnesota’s proposed expansion of its sales tax base illustrate a growing split between states attempting to tax modern advertising models and businesses pushing back on constitutional and federal preemption grounds.

Blogs and Bits

Welcome to March bracket time - Kay Bell, Don't Mess With Taxes:

But what matters at final tax calculation time is your effective tax bracket. As the name indicates, it’s the lower tax rate you really, effectively pay.

Time Running Out To Claim Refunds Owed for 2022 - WHY? - Annette Nellen, 21st Century Taxation: "I have blogged on this a few times before including in 2023 suggesting that a modern system should prevent this situation. For example, why not change the law to allow the IRS to issue the refund?"

Social Security Should Be a Forced Savings Program Not a Welfare Program - Alex Tabarrok, Marginal Revolution. "There is a growing movement to eliminate the wage cap on Social Security taxes while capping benefits. The argument, often from the center-right, is that Social Security is insolvent and that 'tough' choices are needed to save it. But this moves the system in exactly the wrong direction."

A Family Business

Family Members Get Prison Terms For Tax Refund Scheme - Anna Scott Ferrell, Law360 Tax Authority ($):

From a Department of Justice press release issued when the taxpayers were convicted (Defendant names omitted, emphasis added):

Collectively, the defendants received over $1.7 million from the IRS based on the false tax returns they filed. Court records reflect that the defendants shared in the proceeds of their fraud by transferring money between themselves. They also used the refunds to purchase luxury goods, furniture, cryptocurrency, a Cadillac Escalade, and a house in Mississippi.

Like many cunning plans, this worked out great, until it catastrophically did not. Getting illegal refunds can be a lot easier than keeping them.

What day is it?

It's National Pencil Day! A good day to revisit the pencil's classic ghost-written autobiography. "I, Pencil, simple though I appear to be, merit your wonder and awe, a claim I shall attempt to prove."