Key Takeaways

- Treasury Secretary ignores taxwriter questions on slow paper refunds.

- Notices don't outline 10-week delay.

- Overtime confusion in filing season.

- IRS lost AI specialists in DOGE cuts.

- How tax agencies are using AI tools.

- Moving abroad and US taxes.

- International Waffle Day.

Missed Deadline for Treasury to Address Refund Delays Riles Dems - Tyrah Burris, Tax Notes ($):

A second letter from Reps. Danny K. Davis, D-Ill., and Terri A. Sewell., D-Ala., presents additional concerns about the tax refund delays and requests that Bessent provide information on the IRS notices sent to taxpayers explaining that their refunds couldn’t be processed via direct deposit without updated direct deposit information.

...

In both letters, the lawmakers expressed concern that the notice doesn’t clearly state that taxpayers could face more than a 10-week delay in receiving their paper refund and that the IRS doesn’t provide a process for taxpayers who lack an online account to receive a check.

No Tax on Overtime in the 2026 Filing Season - Aaron Till and Andrew Lautz, Bipartisan Policy Center:

One Big Beautiful Bill: What We Know So Far - William Gale, Benjamin Page, Elena Spatoulas Patel, and Joseph Rosenberg, TaxVox:

For comparison, the fiscal resources spent in the OBBBA would have been sufficient to resolve Social Security’s long-term financing problem.

IRS Income Tax Refund Schedule 2026: When Will Your Refund Arrive? - Kate Schubel, Kiplinger. "It’s also important to note that errors in your tax forms, IRS processing delays or bank delays might extend the waiting period for your tax refund."

IRS Staffing Issues Plague AI adoption: Watchdog

IRS Must Address AI Skills Gaps, GAO Says - Asha Glover, Law360 Tax Authority ($):

AI has significantly benefited the IRS by leading to advancements in potential fraud detection, and it has the capacity to increase the government's effectiveness and efficiency, according to the GAO's report. The tax agency had 126 active AI applications for specific business purposes as of June, and increased AI use has been a goal at the IRS, the GAO said.

However, the agency's workforce has been significantly reduced since 2025, and that could have a significant effect on its ability to use AI, according to the GAO. According to the report, 63 employees in the agency's research, applied analytics and statistics group who were working on AI are no longer at the agency, and other IRS units that support AI efforts also have lower employment numbers compared with January 2025.

Staff Losses Hamper IRS Artificial Intelligence Agenda, GAO Says - Benjamin Valdez, Tax Notes ($):

The GAO said AI governance officials at the IRS haven’t had any formal conversations with the IRS Human Capital Office or other divisions to identify staffing needs or address them. Short-term hiring plans are focused on customer service and audit employees, not employees with AI expertise, the watchdog said.

The loss of procurement staff who were familiar with technical AI contracts quickly manifested between February and June 2025, when officials struggled to respond to “repeated requests” from the Department of Government Efficiency to justify contracts, the GAO said.

Tax Agencies Using AI Mainly To Flag Fraud, OECD Says - Natalie Olivo, Law360 Tax Authority ($):

...

For tax administrations that use AI to identify suspicious returns for audits, problems with underlying data — including how AI is trained on it — have led to scandals in the past.

The Netherlands' tax authority made international headlines in 2019 when the Dutch state secretary for finance resigned amid criticism of his office's role in demanding repayment from families of child tax benefits that were wrongly canceled. According to a government investigation, the tax authority had relied on an AI algorithm that used dubious criteria — such as whether parents had dual citizenship — that stopped payments to thousands of parents.

Tax Policy: What's Different for Dems; Whistleblower Bill

What’s Different About the Latest Democratic Tax Plans? - Katie Lobosco, Tax Notes ($):

They still want to tax the rich. And they still want to expand the child tax credit. But there’s a new focus on ending federal income taxes for millions of middle-income people.

...

There’s another reason Democrats may not make middle-income tax cuts a priority even if they win control of the White House and Congress. A tax cut may leave less money for the many programs Democrats wish to fund, like restoring cuts to Medicaid, the expired Affordable Care Act tax credit, and the clean energy tax credits phased out by OBBBA, to name a few.

House Tax Writers to Consider IRS Whistleblower Bill - Naomi Jagoda, Bloomberg ($):

The whistleblower bill would make changes that include expanding the US Tax Court’s ability to review IRS whistleblower award determinations and giving whistleblowers a presumption of anonymity before the court. The provisions in the bill also are included in a wide-ranging tax administration package introduced in the Senate by Finance Committee Chair Mike Crapo (R-Idaho) and ranking member Ron Wyden (D-Ore.).

Other bills slated for consideration by Ways and Means Wednesday would require the IRS to create a dashboard to keep taxpayers informed about backlogs and wait times, provide tax relief to those affected by wildfires and other disasters, allow early childhood educators to be eligible for a deduction for education expenses, and prevent survivors of sexual abuse from having to pay taxes on settlement income.

Travel Plans?

What Americans moving to the UK need to know about tax - Clare Maurice, Financial Times:

Most of the clients I see moving to the UK have already established a sophisticated estate plan, but unsurprisingly this is US driven. They are set up with revocable trusts, pour-over trusts, durable powers of attorney and healthcare directives, to name but a few. More often than not, in the UK these arrangements are at best ineffective and at worst generate unwanted tax consequences. Whichever, there will be confusion. It is essential these should be reviewed.

Related: Eide Bailly Global Mobility Services.

Renounce U.S. Citizenship Fee Cut To $450—But Tax Traps Remain - Virginia La Torre Jeker, US Tax Talk:

Dividend Tax Rates in Europe, 2026 - Cristina Enache, Tax Foundation Europe:

Estonia, Latvia, and Malta are the only European countries covered that do not levy a tax on dividend income. For Estonia and Latvia, this is due to their cash-flow-based corporate tax system: instead of levying a dividend tax, they levy a corporate income tax of 22 and 20 percent, respectively, when a business distributes its profits to shareholders. Malta, in contrast, allows shareholders to offset personal income tax on their dividend income against its 35 percent corporate tax rate, resulting in a zero percent top rate.

...

For comparison, the United States applies a combined state and federal dividend tax rate of 28.73 percent.

State Taxes: Incentives; Property Taxes

SALT Credits & Incentives: The Playbook - Part III - Colette Sutton and Matt Carlson, Eide Bailly:

Ending Property Taxes Would Be a Mistake - Judge Glock, City Journal:

The likely alternative—centralization of taxes at the state level, especially through higher income and sales taxes—would undermine growth. That’s because local governments are more favorable to growth when they can absorb its fiscal benefits through property taxes. A study in the Journal of Housing Economics found that countries with centralized finances tended to restrict housing growth. Countries that allowed local governments to keep more revenue, by contrast, permitted more development.

Blogs and Bits

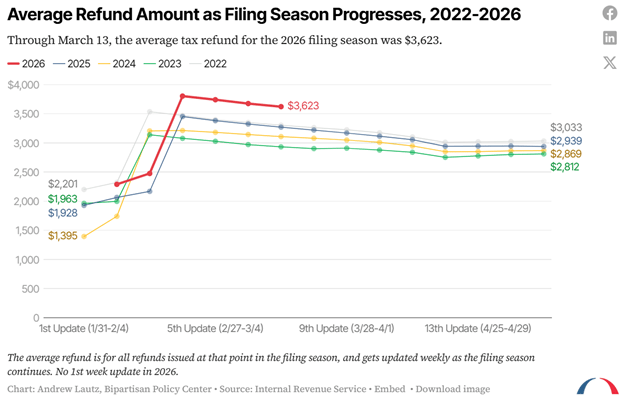

Bigger refunds are real but the $1,000 claim looks far off - Adam Parr, Tax Coda: "The IRS reports that average refunds reached $3,623 for returns processed through March 13, 2026, a 10.8% increase from $3,271 at the same point last year. While this is a significant rise, it is about $350 higher, not the $1,000 increase promoted by the White House and President Trump."

DOL Proposes New Independent Contractor Rule - Kristiana Coutu, Ag Docket. "Employers have significant responsibilities under the FLSA in relation to their employees. These obligations do not apply when hiring an independent contractor who is in business for themselves and providing services in that capacity."

IRS Was Correct to Use Deficiency Procedures in Collecting Erroneous Refund - Parker Tax Pro Library. "The Tax Court held that the erroneous portion of a refund that the IRS issued to a taxpayer was a rebate refund, and not a nonrebate refund as argued by the taxpayer, and thus could be collected from the taxpayer through deficiency procedures."

You Don't Want to Have a Business on Your 1040 if You Don't Have a Business

San Joaquin County woman sentenced to 18 months in prison for defrauding the IRS of over $1.2 million - IRS (Defendant name omitted, emphasis added):

Defendant was sentenced today to 18 months in prison for two counts of aiding or assisting in the preparation or presentation of a false or fraudulent tax return, U.S. Attorney Eric Grant announced.

...

According to court documents, for the tax years from 2017 through 2020, Defendant falsified more than a thousand of her clients’ tax returns to increase the refund amounts without her clients’ knowledge or consent. Defendant reported false businesses, false income, and false expenses for her clients to the Internal Revenue Service. In one instance, Defendant prepared a client’s 2019 tax return and falsely reported $8,830 in business losses when the client did not operate any business in 2019, nor had she told Defendant that she operated any business or had any business expenses. Additionally, there were no business records to support the false tax schedule filing except for a fraudulent Form 1099-MISC that was prepared for the client. Defendant repeated similar conduct with respect to hundreds of her clients.

"Without her clients' knowledge or consent" raises questions. I would guess that the defendant built a client following from generating big refunds, and that the clients didn't look too closely at how the refunds came about.

We are all responsible for our own 1040s. Look yours over before you sign, especially if you suddenly are getting a windfall.

Courts have ruled that the statute of limitations never starts to run if your return was fraudulently prepared - even if you didn't know the preparer was committing fraud. Be careful out there.

What day is it?

It's International Waffle Day, a glorious day bursting with butter and maple syrup!