Key Takeaways

- Fraud concerns help slow down paper check tax refunds.

- Refund increase so far falling short of expectations.

- Undistributed capital gain scams.

- Claude, ChatGPT aren't ready to do your taxes.

- Study says charities will suffer from Trump tax changes.

- Own nothing, control everything tax fail.

- National Sloppy Joe Day.

Really Big Show Today! If you are a business owner, you want to catch Before Your Sell: How Early Wealth Transition & Estate Tax Planning Determines Your Net Outcome. Presented by Eide Bailly's Devin Hecht and Bob Clark, the session covers what you can do now to ensure the best results when the day comes to cash out of your business, or to transfer it to the next generation. Today at 2 pm Central. Register here.

Filing Season Update: Refund Backup, Refund Bump

Fraud Worries Complicate IRS Push to Halt Paper Refunds - Benjamin Valdez, Tax Notes ($):

Some of the confusing features of the CP53E notice, which is being sent by the IRS to taxpayers without direct deposit, are the result of the agency trying to deter taxpayers from calling and providing their sensitive financial information, Collins told Tax Notes during a March 17 event hosted by the Tax Executives Institute.

IRS assisters can’t accept taxpayers’ bank account information for security reasons, according to Collins, so the notice includes a phone number that only provides an explanation of the notice but doesn’t offer a way to transfer to other IRS customer service lines.

At the same time, taxpayers without a bank account or online IRS account will need to call the IRS’s dedicated phone line — a phone number not listed on the notice — to request an exception to obtain a paper refund check.

Again: E-file if you can. Include bank account information if you have it. Be sure key information - tax payments, W-2 amounts, 1099 items - is correct. And if you have college-age dependents, make sure they don't file as non-dependents. Missing any of these items can hold up your return and refund processing for months.

Could there be a further refund bump? - Bernie Becker, Politico:

...

It seems pretty clear then that Republicans have succeeded in driving up tax refunds this year, by making the new deductions from last year’s megabill on tipped income, overtime pay and new car loan interest, among other tax cuts, retroactive to the beginning of 2025. (Not to mention: Declining to update withholding tables last year, ensuring that the new tax relief would pile up in filing season.)

But with not even a month now remaining until April 15, it’s also fair to question whether the Republican tax cuts have essentially maxed out what they can deliver in refunds — and with the increase in average payment stuck at around $350 for several weeks, well short of the $1,000 hike that the GOP promised.

Scams and AI Errors

IRS Flags Growing Scam Linked to Undistributed Capital Gains - Tyrah Burris, Tax Notes ($):

The schemes involve an overstated or fabricated Form 2439, “Notice to Shareholder of Undistributed Long-Term Capital Gains,” which allows shareholders of certain investment funds or real estate trusts to claim a credit for taxes paid on undistributed capital gains.

Claude, ChatGPT Tackle Taxes Even as Pros Warn of Costly Errors - Ben Steverman and Charlie Wells, Bloomberg ($):

But modern LLMs have capabilities that can help compensate for their shortcomings. Some of the accountants who complain most loudly about AI are the ones who use it the most—including Scott, who says he’s careful to check all its work. He also relies on AI to develop his internet marketing content. Nayo Carter-Gray, owner of 1st Step Accounting in Baltimore, uses it to walk clients through difficult concepts, such as “breaking down what depreciation is,” she says. Given the weaknesses of LLMs, Michael Geller, a partner at Gursey Schneider in Los Angeles, says, “I’m not afraid of it taking my job.” Still, he urges colleagues to adopt AI as “a new tool to do things quicker than before.”

AI tools will continue to improve. Given the complexity of the tax law and the aging of tax preparers, especially in rural areas, AI tools will become an essential part of tax compliance in the coming years. Even so, they are a long way from displacing humans.

Charities Will Be Tax Losers, Says Study

Charities Face Projected $5.7 Billion Yearly Hit From Tax Change - Ben Steverman and Caitlin Reilly, Bloomberg ($):

Overall, funding to charity is likely to drop by $5.7 billion per year from the law, the research finds, despite a new deduction encouraging millions of Americans to give.

The new rules shrink incentives for corporations and rich Americans to give to charity by reducing the amounts they’re allowed to deduct in various ways. Combined, three provisions affecting these deep-pocketed donors are likely to cost nonprofits $10 billion annually before accounting for any offsets that might occur, the study finds.

OBBBA Will Cut Charitable Giving by $5.7B Annually, Report Says - Kelsey Brooks, Tax Notes ($):

The OBBBA also amended section 68 to establish a 35 percent cap on the value of charitable deductions for individual taxpayers in the 37 percent tax rate bracket. That provision alone will lead to a roughly $6.1 billion decrease in charitable giving annually, according to the report, “The Philanthropy Outlook: Estimating Effects on Charitable Giving From the One Big Beautiful Bill.”

“Changes that affect high-income households and large corporate donors have the greatest influence on total giving levels,” Patrick Rooney of the Lilly Family School of Philanthropy said in a release.

Teeing up the Next Round of Tariffs

After IEEPA: What New Section 301 Investigations Mean And Why Public Input Matters - Kari Heerman and Elena Spatoulas Patel, TaxVox:

...

But unlike IEEPA, Section 301 requires a formal investigative process—including written submissions and public hearings—before tariffs can be imposed. Although it requires no additional congressional approval, Section 301 does require public notice, the development of an administrative record, and a legal determination before action is taken. This gives businesses, workers, and other stakeholders the opportunity to shape the factual and legal record on which any tariffs will rest.

States Seek To Block Trump's Latest 10% Tariff Order - Kat Lucero, Law360 Tax Authority ($):

Trump ordered the tariffs under Section 122 of the Trade Act of 1974 without tying them to U.S. international payment problems as required by the statute, the coalition of states said in a motion seeking summary judgment or a preliminary injunction. In addition, they said, the order's product exemptions violate its nondiscrimination requirement.

The president's "attempt to exercise enormous tariff authority and the implementation of his proclamation exceeds Section 122's limits and violates the separation of powers," the coalition said, noting that Section 122 has never been invoked until now.

Red and Blue Tax Policy

Red and Blue States Are Growing Further Apart on Income Tax - Richard Rubin and Jeanne Whalen, Wall Street Journal:

Republican-led states are racing each other to flatten, cut and eliminate individual income taxes, with 23 states lowering their top income-tax rates since 2021. Mississippi and Oklahoma, among others, put themselves on paths to eliminate personal income taxes. South Carolina is setting a course this year to drop its top income-tax rate to 1.99%, and Missouri residents may vote this November on a plan to phase out income taxes and allow lawmakers to expand sales taxes.

Democratic-controlled states are moving the opposite way, pushing to increase taxes on top earners to combat inequality and plug budget holes expected from Republicans’ cuts to federal health and nutrition assistance programs. Washington state’s legislature last week sent Gov. Bob Ferguson a bill that would create a 9.9% income tax on earnings over $1 million. New York City Mayor Zohran Mamdani is pushing state lawmakers to raise income taxes on high-income households.

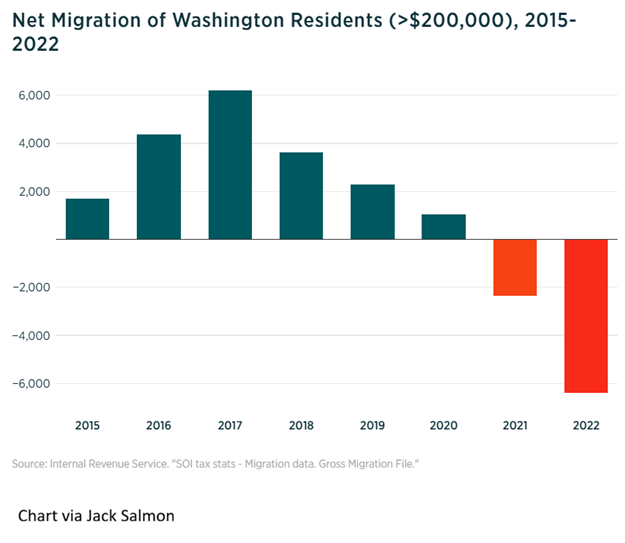

Blue States Are Chasing Away Their Tax Bases: A Surge in Taxes on High Earners Is Leading to a Mass Exodus - Jack Salmon, The Unseen and The Unsaid:

...

The chart below shows the net migration of earners making more than $200,000 between 2015 and 2022. Over 2,300 high earners left the state on net in 2021, the year the 7% tax was enacted, and almost 6,400 more left in 2022 when the tax came into effect.

Taxes aren't everything. They are a thing.

Tax Incentives are Red and Blue

SALT Credits & Incentives: The Playbook - Part II - Colette Sutton and Matt Carlson, Eide Bailly:

In practice, incentive value is often driven more by up‑front facility investment than by ongoing wages. As a result, a $50 million manufacturing facility with moderate hiring can generate greater total incentives than a $5 million office project with higher wages once programs are fully modeled. Well‑known examples include the Georgia Job Tax Credit, Kansas’s PEAK (Promoting Employment Across Kansas) program, and the Texas Enterprise Zone Program.

Blogs and Bits

Don’t miss these 10 often-overlooked tax breaks - Kay Bell, Don't Mess With Taxes. "Here are 10 tax breaks you definitely should investigate before sending your 1040 to the Internal Revenue Service."

The nation’s accelerating self-assassination - George Will, Washington Post. "Longevity is a social triumph. But in the context of increasingly competent (and expensive) medicine, and an entitlement state, it can be ruinous. And is regressive: It involves huge annual transfers of wealth upward from current workers to retirees who, after lifetimes of accumulation, are more affluent than their younger benefactors."

Understanding Demonic Policies - Alex Tabarrok, Marginal Revolution:

"Own Nothing, Control Everything" Fail

Tax shelter promoters plead guilty to conspiracy to defraud the United States - IRS (Defendant names removed, emphasis added):

Defendant contributed to the filing of at least 321 false tax returns, which concealed more than $27 million in client income and $3.7 million of his own income. His crimes caused more than $8.7 million in losses to the United States.

"Own nothing, control everything." It sounds sophisticated. The clients were sure it worked, and probably bragged about it to their friends. Then one day it didn't. The defendant isn't going to pay the back taxes owed by his clients. The IRS is surely working its way through Defendant's client list. Current Tax Court precedent says they have forever to do it, with no statute of limitations.

What day is it?

It's National Sloppy Joe Day! Remember to use a napkin.