TIGTA Continues to Hammer IRS’s Taxpayer Experience Team - Jonathan Curry, Tax Notes ($):

A TIGTA report released June 5 describes an organizational structure in flux at a critical time for the agency as it tries to implement changes. The report concludes that the IRS not only lacks a comprehensive strategy for improving services for underserved communities but also still hasn’t defined who comprises those various communities.

The report, dated May 31, comes on the heels of one released two weeks earlier by TIGTA, which similarly concluded that the newly formed Taxpayer Experience Office (TEO) was falling short of expectations, both in hiring staff and in coordinating initiatives across the agency’s divisions.

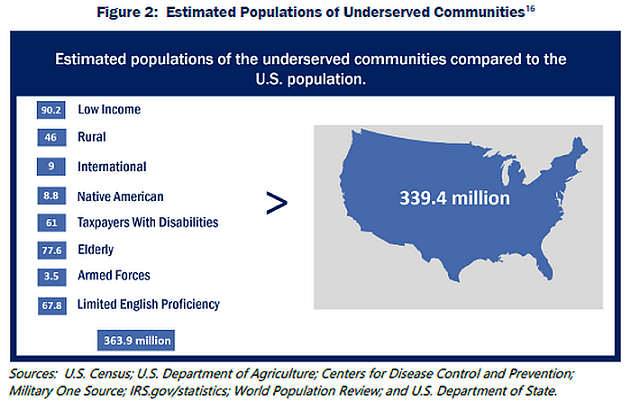

The report says the office was launched in March 2022. This passage and chart from the report, combined with an illustration, is interesting:

Figure 2 shows that when counted separately, the populations of underserved communities combined exceed the population of the entire country, highlighting the potential for overlap among underserved communities.

Then again, there is a plausible argument that when it comes to tax administration, we are all underserved and then some.

Oklahoma Tax Bills Become Law Without Governor’s Signature - Emily Hollingsworth, Tax Notes ($):

H.B. 1039 eliminates the annual corporate franchise tax for tax years beginning on or after January 1, 2024. The tax, which applies to corporations, associations, joint stock companies, and business trusts that do business in the state, is levied at $1.25 for each $1,000 of capital invested or used in the state.

H.B. 1040 increased from $12,200 to $14,400 the upper threshold for the 3.75 percent income tax rate for joint filers, heads of household, and surviving spouses. The top income tax rate of 4.75 percent would apply to those taxpayers' income over $14,400. The adjustment brings that threshold to exactly double the one for single filers and those who are married filing separately, as all the other joint filers' income thresholds already were.

Justices Send Nebraska Tax Sale Cases Back to State High Court - Perry Cooper, Bloomberg ($):

The cases sent back were filed by homeowners Kevin Fair and Sandra Nieveen, who challenged Nebraska’s law that allowed a private third party to seize Fair’s home worth $60,000 over a $588 tax deficiency and Nieveen’s home worth $61,000 over $3,796. The Nebraska Supreme Court upheld both sales.

The justices didn’t explain why they sent the cases back, but presumably it was to apply the court’s May 25 holding Tyler v. Hennepin County that local governments commit unconstitutional takings when they keep surplus proceeds after a homeowner’s property is seized and sold due to delinquent taxes.

Income Tax Economic Nexus Is Open Question Post-Wayfair - Maria Koklanaris, Law360 Tax Authority ($):

After the U.S. Supreme Court's 2018 decision in South Dakota v. Wayfair set off a wave of economic nexus sales tax laws and then another of marketplace facilitator laws, many observers expected states would next turn to establishing thresholds for the corporate income tax. A few did, including Hawaii, Pennsylvania and Texas, and Louisiana has a pending bill to do so. All told, though, fewer than a third of states set forth specific dollar standards that tell businesses when economic nexus is triggered for the corporate income or franchise tax, relying instead on a vague so-called doing-business standard.

That makes it a challenge to determine which states a business must file income tax returns:

Similarly, the major cases from state high courts are all more than 15 years old. It is difficult to apply any of them to current conditions, since more than 30 states now use sales-factor-only apportionment, and another 10 consider other factors but put additional weight on the sales factor, said John Gupta, state and local tax practice leader at Eide Bailly LLP.

Related: Eide Bailly State & Local Tax Services.

Market for Sellable Green Tax Credits Heats Up Ahead of IRS Rule - Erin Slowey and Isabel Gottlieb, Bloomberg ($):

The Inflation Reduction Act-created new market for green energy credits that can be directly bought and sold is a key piece of the US’s clean energy transition. The existing method green energy developers use to monetize their credits is a nearly tapped-out market with barriers to entry for smaller players. The new method, known as transferability, is expected to significantly expand the pipeline of investment flowing into new renewables.

...

The IRA lets developers directly sell certain tax credits one time. It is meant to appeal to a broad range of sellers, from the smallest clean-energy projects to larger developers, such as regional utilities companies, and buyers—any company that wants to offset some of its taxes.

Why Employees Should Have an IRA Separate From Their Work 401(k) - Michael Pollock, Wall Street Journal. "It is true that having an IRA alongside a company plan would add complexity to someone’s financial life, but there are a number of potential future benefits. For one thing, IRAs open a wider range of investment choices than those typically found in company plans. And, depending on the account, they could enable a saver to defer taxes on significantly more income—or stash away money that might be tax-free when withdrawn in retirement."

IRS battles coverup accusations in Tax Court - Benjamin Guggenheim, Politico. "The case involves a partnership that claimed tax breaks for conservation deals and accuses the IRS of engaging in a coverup of a mishandling of documents by the agency that could make a difference of millions of dollars of penalties assessed against the taxpayer."

IRS budget battle not over after debt ceiling agreement - Laura Weiss, Roll Call. "Republicans are vowing to continue attempts to chip away at the roughly $59 billion in IRS funding that will remain, if the handshake agreement holds."

Summer's here, meaning it's time for June tax moves - Kay Bell, Don't Mess With Taxes. "June 15 also is another Tax Day for millions of folks who get income that isn't subject to withholding taxes. This mid-June deadline is for the second payment due on such income received this April and May. You can get more scoop on estimated taxes and timetables in my estimated tax primer. You also can check out my earlier posts on estimated tax questions and answers and why, when, and how to pay estimated taxes."

More on reliance on a tax professional for penalty relief - Thomas Gorcyzynksi, Tom Talks Taxes. "In closing, when a taxpayer is assessed a penalty for failing to file a tax return, and the preparer failed to file an extension as expected, or electronically transmit a return that the taxpayer authorized, there currently is no case law supporting relief using reliance on a tax professional."

Tax Court Finds Elderly Attorney Qualified for Reasonable Cause Exception for Late Filing and Late Payment - Ed Zollars, Current Federal Tax Developments. "Typically, a taxpayer will not be deemed to have exercised ordinary business care and prudence if they merely delegate actions to a third party but fail to adequately oversee and supervise the actions of that party to ensure the fulfillment of the obligation."

AI Technology Could Help IRS Recover $600 Billion - Rebekah Barton, TaxBuzz. "It is worth noting that the IRS already uses artificial intelligence in some capacity. The government agency has partnered with IBM to automate its existing e-File system, which is likely to be revamped in the upcoming months and years."

Charity loses exempt status over contract with related for-profit organization - National Association of Tax Professionals. "In this instance, the charity had contracted with a management services organization (MSO) operated by a former officer and his wife without seeking competitive bids."

Bicycling and Tax Breaks - Annette Nellen, 21st Century Taxation. "If a tax break is to be provided, why not offer a refundable credit for the purchase or a bike with reasonable cost limits and an income phase-out level? "

R&D Amortization Hurts Economic Growth, Growth Industries, and Small Businesses - Alex Muresianu, Tax Policy Blog. "Making taxpayers spread research and development deductions out means that companies cannot deduct the full cost of investment thanks to inflation and opportunity cost. Companies value present deductions more than future deductions because a deduction now means tax savings can be reinvested. Under the half-year convention, assuming a 3 percent discount rate and 2 percent inflation, companies would only be able to deduct 88.3 percent of domestic R&D investment. Higher inflation means an even larger tax penalty: under 5 percent inflation, a company could deduct just 82.8 percent of its costs."

Does the “Chicken Tax” encourage people to purchase larger trucks? - Robert McClelland, TaxVox. "Another factor beyond the Chicken Tax is the Corporate Average Fuel Efficiency (CAFE) standards manufacturers must meet with their entire fleet of vehicles. CAFE standards have always been lower for trucks, and since 2011 the standard has been based on the “footprint” of the vehicle. This means that larger trucks face lower mileage requirements than smaller trucks. Absent this change, manufacturers may not have been able to produce larger trucks while still meeting CAFE standards."

Individuals Barred from Promoting CRAT Tax Shelter Scheme - Thomson Reuters Tax & Accounting:

A federal district court in Missouri has barred several individuals and Hoffman Associates, LLC, from promoting, selling, or marketing a tax shelter scheme involving the use of charitable remainder annuity trusts (CRAT). According to court records, the defendants falsely claimed that, by using their CRAT scheme, taxpayers could sell property and avoid paying federal income tax on any gain generated by the sale.

...

The promoters recruited participants to their scheme by advertising in local newspapers, using online platforms and the Hoffman Associates website. Once a participant signed on to the scheme, the promoters created a CRAT. The participant then contributed property (usually appreciated real property) to the CRAT. After the property transfer, the promoters would sell the property and use most of the proceeds to purchase an annuity for the participant. Finally, the promoters falsely reported the annuity payments received by the participant as a tax-free distribution from the CRAT. As a result, neither the CRAT nor the participant pay tax on any gain from the sale of the contributed property.

This scheme made the IRS "dirty dozen" scam list.

Link: Injunction order.

Ottumwa Man and Woman Convicted for Filing Hundreds of False Tax Returns and Fraudulently Obtaining Unemployment Insurance Benefits Payments - US Department of Justice (defendant names omitted):

According to court documents and evidence presented at Mi’s four-day trial, Defendants ran a fraudulent tax-preparation business out of their family’s Ottumwa home. In exchange for a cash fee, Defendants prepared and filed their customers’ tax returns. Defendants primarily catered to immigrants and refugees who worked at meat-packing facilities in Iowa and who had little or no ability to read, write, or speak English.

Without their customers’ knowledge or approval, Defendants included on their customers’ federal tax returns, schedules, and forms, fraudulent items, such as false claims for residential energy credits, business-expense deductions, or moving-expense deductions for members of the United States Armed Forces. The effect of Defendants including fraudulent items on the tax documents was to increase the refunds their clients received and increase Defendants’ customer base. In all, from 2018 to 2022, Defendants caused over 1600 tax returns to be filed from their Ottumwa residence. The fraudulent tax returns claimed over $3.5 million in residential energy credits.

From 2018 to 2022, Defendants received approximately over $200,000 in cash fees from their customers. In addition, on their customers’ returns, Defendants sometimes directed portions of the fraudulent refunds be sent to financial institution accounts accessible to Defendants.

The tax law can seem like a foreign language to many native English speakers. Imagine having to deal with it without being fluent in English. It's not surprising that tax scammers prey on immigrants.

We all have our ups and downs. It's National Yo-Yo Day!