Telecommuting Boom Puts Employers at Risk for Millions in Taxes - Sam McQuillan, Bloomberg Tax. "Companies are generally responsible for witholding payroll taxes for any salary an employee earns while working in a jurisdiction. Unless they track their employees—and many don’t—they won’t know about their liability unless the workers themselves alert them to location changes."

Connecticut General Assembly Passes Remote Worker Tax Credit Bill - Lauren Loricchio, Tax Notes:

The bill's remote worker provisions would apply for the 2020 tax year and would take effect upon enactment of the bill. It would allow Connecticut residents who paid income tax to another state with a convenience of the employer rule in place to obtain an income tax credit for the amount paid to the other state.

The neighboring state of New York has a convenience of the employer rule, which requires a nonresident taxpayer’s income to be sourced to the employee’s physical location while working remotely by necessity and to be sourced to the employer’s location if the employee is working remotely for convenience.

IRS warns: Stop taking this deduction — it’s been repealed - Jeff Stimpson, Accounting Today. The Internal Revenue Service has issued an alert concerning amended returns and claims for the Domestic Production Activities Deduction.

This refers to the old Section 199 producer's deduction repealed after 2017. It does not refer to the newer Sec. 199A(g) deduction for cooperatives and their farm patrons, which is often informally referred to as the "DPAD" deduction; that deduction remains in effect.

Tax Time Guide: Didn’t get Economic Impact Payments? Check eligibility for Recovery Rebate Credit - IRS. "Individuals will need to know the amount of their Economic Impact Payments to claim the Recovery Rebate Credit. Those who don't have their Economic Impact Payment notices can view the amounts of their first and second Economic Impact Payments through their individual online account. For married filing joint individuals, each spouse will need to log into his or her own account."

IRS Notice Indicates How to Determine ERC Eligible Wages Deemed Used to Obtain PPP Loan Forgiveness in 2020 - Ed Zollars, Current Federal Tax Developments. "This guidance is limited to the 2020 version of the ERC, and does not take into account changes that took effect on January 1, 2021."

IRS announces underpayment, overpayment rates for 2021 Second Quarter - Eide Bailly Tax News & Views. Interest rates are unchanged from first quarter. 3% rate continues to apply for estimated tax underpayment penalties.

Wolters Kluwer Examines the Tax Provisions of the American Rescue Plan Act - Wolters Kluwer Tax & Accounting Blog. "In many cases, the proposed tax provisions of the American Rescue Plan Act are extensions or expansions of existing tax law to provide some immediate assistance to individuals and businesses affected by the pandemic."

Section 911 Housing Cost Amounts Updated for 2021 - International Tax Blog. "For example, the limitation on Housing Expenses for 2021 in Bern, Switzerland is $72,900. Therefore, an individual living in Bern with housing expenses in 2021 of $72,900 or more could exclude from income an amount of $55,508 ($72,900 - [108,700 X 16%])."

Related: Considering Foreign Operations? You Need a Global Mobility Program.

Paying self-employment taxes on the revised Schedule SE - Kay Bell, Don't Mess With Taxes. "Schedule SE is the self-employment answer to the Federal Insurance Contributions Act (FICA) payroll taxes taken out of a worker's salary. FICA tax amounts go toward the Social Security and Medicare programs, with workers and their bosses each paying an equal amount of tax that is calculated as a percentage of a worker's salary."

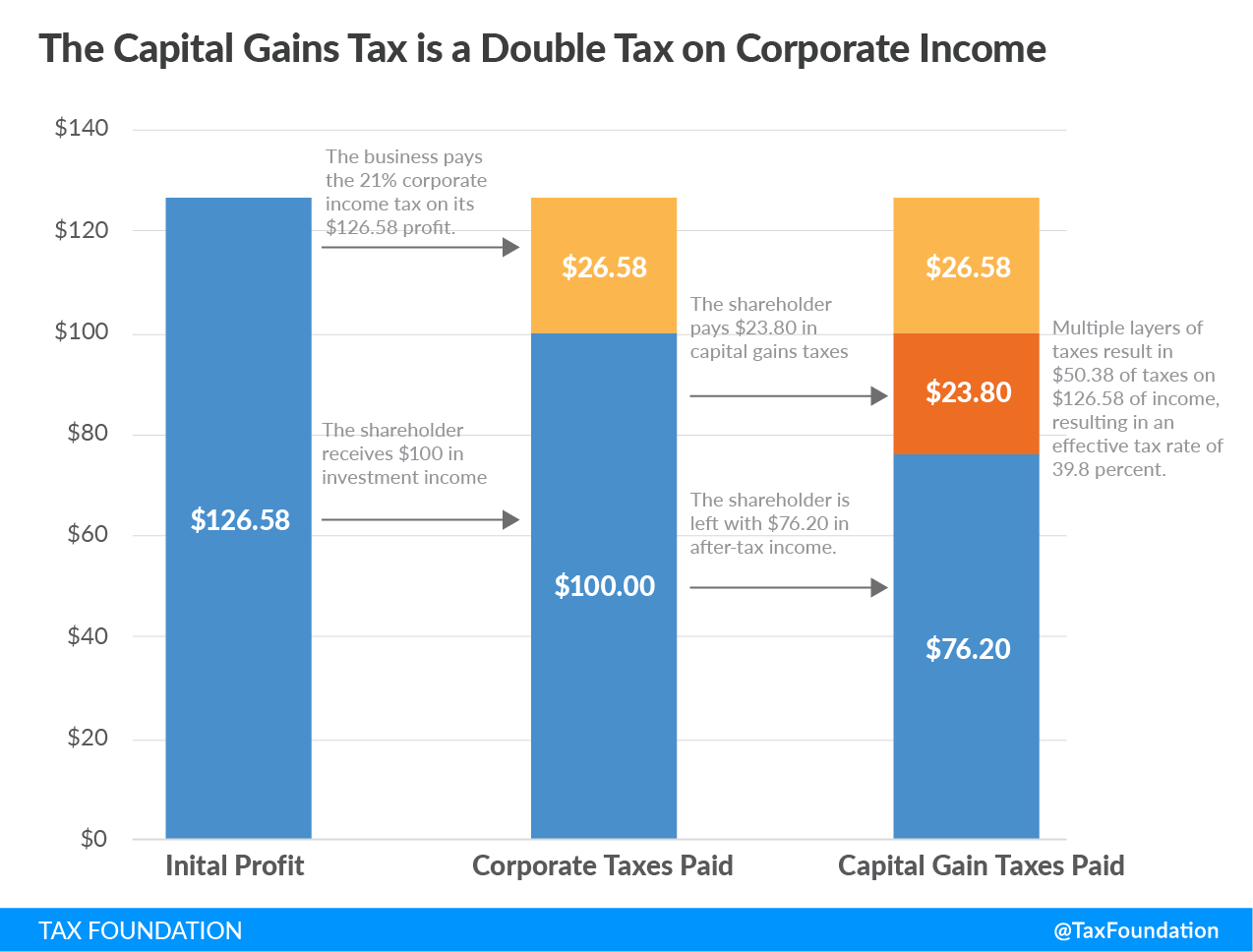

Sen. Elizabeth Warren’s Wealth Tax Legislation Faces Administrative and Economic Challenges - Erica York, Tax Policy Blog:

Compared to income taxes, wealth tax rates seem much lower, but that perception can be deceptive. The best way to interpret wealth tax rates is to translate them into an equivalent income tax rate. Imagine an investor who owns a long-term bond with a 5 percent fixed rate of return each year. A 3 percent annual wealth tax implies that 60 percent of the income flow from the bond would be remitted as tax. The 60 percent tax on the return to wealth would be in addition to other layers of tax that capital income faces under current law, including federal, state, and local corporate income taxes, individual income taxes on interest income, capital gains, and dividends, and estate and gift taxes...

Several countries in the Organisation for Economic Co-operation and Development (OECD), including Austria, Denmark, Germany, Finland, Iceland, Luxemburg, Ireland, and Sweden, chose to repeal their wealth tax during the last 30 years. The tax policy literature indicates reasons for repeal include limited revenue collection, administration and compliance cost, tax avoidance, and evasion.

{kind=link}

There's Lots to Like in the Like-Kind Exchange Regs - Marie Sapirie, Tax Notes Opinions.

One of the open questions following the final rules’ inclusion of specific types of intangibles in the definition of real property is the scope of the items on the “in” list. Under the final rules, options to acquire real property are now within the definition, along with more obvious interests like fee ownership, co-ownership, leases, and easements. The regulations include a catchall for “similar interests,” as long as the “intangible derives its value from real property and is inseparable from that real property or interest in real property.”

Related: Section 1031 Like-Kind Exchanges: 98 Years Old, Powerful and Tricky

Aretha Franklin’s Estate and IRS Reach Deal on Singer’s Tax Woes - Jonathan Curry, Tax Notes:

Under the agreement, which was filed February 19 in Michigan’s Oakland County Probate Court and has yet to be approved by the judge overseeing the case, the estate would make an immediate $800,000 tax payment and reserve 45 percent of all subsequent income it receives from sources such as song royalties and licensing agreements to pay off Franklin’s unpaid income tax liabilities from 2010 to 2017, which the IRS has assessed at $7.8 million. Another 40 percent of future estate revenue would be held in escrow to pay ongoing state and federal taxes owed by the estate and Franklin’s heirs.

The remaining 15%? Four sons would receive $50,000 cash. Then the first $1 million of future income covers estate administrative costs. Then the four sons would split anything after that. A sad lesson in the importance of good financial and estate planning.

Lassoed. How many times have you been told to find a job doing something you love? It might be great advice for personal fulfillment. Unfortunately, a New Mexico taxpayer found out that personal fulfillment needs to be businesslike if you want it to generate tax deductions.

The taxpayer grew a successful insurance sales business, but, having grown up on a ranch, he liked horses. He got hooked on team roping competition, and his tax troubles began. The IRS examiners invoked the so-called "hobby loss" rules prevent taxpayers from deducting losses from activities not carried on for profit.

Tax Court Judge Holmes explains (we omit the taxpayer's real name):

Their “business plan” was simple: They would earn a profit by having Taxpayer “get better” at team roping, by winning team-roping competitions, and also by selling (and possibly breeding) successful team-roping horses. In Mr. Taxpayer's own words, he “wanted to get better, put more effort into it, more time into it, and win.” The values of horses “were a main part” of this plan, and the Taxpayer's claim to have even bought a mare--in addition to their three other horses, “W”, “Rush”, and “Hannaty”--for “the sole purpose of breeding.” But winning was key to making the horses more valuable. “Getting better” also included having the proper equipment, such as a nice saddle and luxury horse trailer that would enable Taxpayers “to go to [the] next level.” The trailer came complete with living quarters, which Taxpayer says ultimately saved him lodging and food expenses while away at roping competitions.

The simple plan didn't pay off in 2009, 2010, of 2011, as the taxpayer showed over $50,000 in losses each year. The taxpayers sought consolation by deducting the losses on their returns. The IRS wasn't in a consoling mood, and things ended up in Tax Court.

Judge Holmes explains the rules to determine if there was a profit objective:

The regulations give us some direction. They say to use “objective standards” to discern a taxpayer’s intent, “taking into account all of the facts and circumstances.” Sec. 1.183-2(a), Income Tax Regs. They give us nine factors to consider, with “[n]o one factor [being] determinative.” They tell us that we can look at other factors not on the list and that we should not make a determination based on the number of factors indicating a lack of profit motive and “vice versa.”

Forbes tax blogger Peter Reilly argues that "only one of the nine factors will either make you or break you." That factor didn't favor the taxpayer here. Judge Holmes again:

The first factor has us look at how the taxpayer carries on the activity. A taxpayer who works in a “businesslike manner” and “maintains complete and accurate books and records” is more likely to have a profit motive... The Taxpayers say that they kept accurate books and records and “carried on the team roping activity in a manner substantially similar to successful team ropers.” To support this they point to Mr. Taxpayer’s weight loss and his rigorous practice schedule, as these factors would improve his performance, and in turn, allow him to win more often.

We do find that Mr. Taxpayer showed considerable discipline and commitment to the sport, but as the Commissioner points out, there are problems with this argument. First, the Taxpayers did not maintain complete and accurate books and records. They never created a budget for team roping, and they didn’t keep track of the money flowing into and out of the activity. Specific proof of this is their largely inaccurate reporting of their 2009 team-roping expenses, and similar inaccuracies for 2010 and 2011. Without adequate recordkeeping, it would be quite difficult for the Taxpayers to evaluate economic performance and ways to improve profitability...

We also think that “winning” without more is not a very believable business plan, especially when the Taxpayers claim to have entered the team roping business because of the insurance market’s volatility. If they were looking for a safer investment, they haven’t found it in winning a team-roping competition here and there.

The other eight factors didn't come out much better, and Judge Holmes came to an unfavorable conclusion:

We find that the Taxpayers did not participate in team roping with the primary motivation to earn a profit... Taxpayer had been team roping for a long time as a hobby before the years at issue. Their business plan was built around “winning”. And the realities of the sport meant that team roping was never going to be a stable source of income for them, especially given its costs. The Commissioner wins on this issue...

The Moral? Vince Lombardi is reputed to have said "Winning isn't everything. It's the only thing." That probably works for football, but for deducting roping losses, good books and records outscore wins and losses.

Link: T.C. Memo. 2021-25

Cheer up! Today is National I Want You to be Happy Day! But if that is too big a stretch, it's also National Cold Cuts Day.