Key Takeaways

- Medical cannabis businesses to get business deductions for entire tax year.

- Treasury announces Sec. 280E guidance process for cannabis rescheduling.

- Judge questions whether a "controversy" exists for Trump $10B IRS suit.

- Is the President too much on both sides of the table?

- This summer's pandemic refund play.

- CA Billionaire tax makes ballot; Illinois millionaire tax fails.

- Marine Mammal Rescue Day.

DOJ Medical Marijuana Order Calls for ‘Retrospective’ Tax Relief - Wesley Elmore and Nathan Richman, Tax Notes ($):

The order doesn’t apply to state-legal recreational marijuana, which remains classified under Schedule I. But it keeps in place the proposed rescheduling rule put forward under former President Biden, which would fully move marijuana under Schedule III, and it kick-starts the stalled hearing process to finalize that rule.

Treasury, IRS Announce Process for Tax Guidance Following DOJ Final Order on Medical Marijuana Rescheduling - US Department of the Treasury (my emphasis):

Section 280E of the Internal Revenue Code generally disallows deductions and credits for any amounts spent in carrying on a business that consists of trafficking in Schedule I or II controlled substances prohibited by federal or state law. Accordingly, rescheduling generally removes section 280E as a bar to claiming deductions and credits for businesses that as a result of the Final Order no longer traffic in Schedule I or II controlled substances under the CSA. Guidance is expected to clarify the ways in which, for businesses with multiple activities, section 280E applies only to those activities related to trafficking in Schedule I or II controlled substances (e.g., by apportioning expenses).

Guidance is also expected to include a transition rule providing that, for purposes of section 280E, rescheduling generally will be considered to first apply for a business’s full taxable year that includes the effective date of the Final Order, for the business’s activities that do not involve Schedule I or II controlled substances as a result of the Final Order.

This means medical cannabis businesses have important relief for the current tax year. The scope and detail of the relief should become clearer when the IRS issues further guidance.

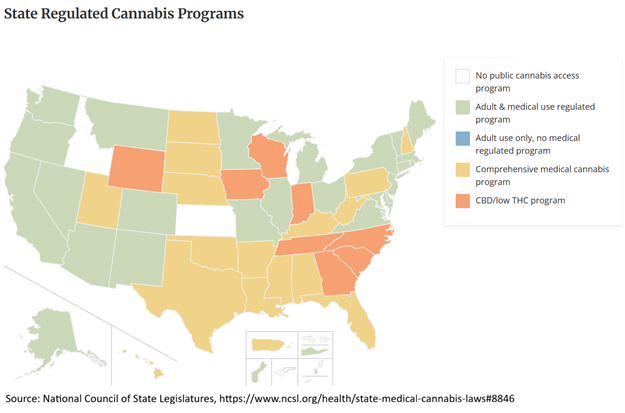

The map below from the National Council of State Legislatures shows the current status of state cannabis laws. Presumably legal businesses in the "comprehensive medical" states will all qualify. Businesses in other states will escape Sec. 280E this year only if they are "medical" sellers.

Judge Questions Ability to Hear Trump $10B Suit v. IRS

Trump’s $10 Billion IRS Suit Hits Snag With Skeptical Judge - Erik Larson, Bloomberg ($):

...

“Although President Trump avers that he is bringing this lawsuit in his personal capacity, he is the sitting president and his named adversaries are entities whose decisions are subject to his direction,” the judge said. “Indeed, President Trump’s own remarks about this matter acknowledge the unique dynamic of this litigation.”

Trump sued in January, alleging the government must pay him damages over a 2020 leak of his tax records to the press. The Justice Department has argued in similar cases over the same leak that the government wasn’t liable.

Williams said it is “unclear to this court whether the parties are sufficiently adverse to each other” to establish her jurisdiction.

The article doesn't discuss what happens if the judge declines to hear the case, or whether the parties can "settle" it if the case can't be heard.

This Summer's Refund Play

Surprise: You May Be Owed An IRS Refund For Payments Made During The Pandemic - Kelly Phillips Erb, Forbes:

The potential extension has opened the door for taxpayers, including individuals and businesses, to recover IRS penalties and interest assessed during the COVID-19 disaster period. For most taxpayers, the deadline to file refund or abatement claims is now July 10, 2026.

...

The Kwong decision is not exactly final. The government can (and likely will) appeal it to the Federal Circuit. If a higher court reverses it, any claim for refund based on the ruling would be denied.

But if you don't file for refund by the deadline and the ruling stands, you are barred from pursuing a claim, meaning even if you're right, you're too late to get your money back.

Related: Eide Bailly IRS Dispute Resolution and Collections Services.

No Summer Tax Bill?

Capitol Hill Recap: Congress Taking a Pass on Tax - Alex Parker, Eide Bailly:

Taxpayer Advocacy Panel Calls for Clearer IRS Notices

...

The six principal project committees presented a series of recommendations to the IRS that include:

- Making taxpayer notices clear, accessible, and easier for taxpayers to understand and act on.

- Enhancing IRS online tools and digital services to expand secure self-service options for taxpayers and improve the user experience within the IRS Online Account and tax transcript applications.

- Streamlining IRS correspondence processes and strengthening Individual Taxpayer Identification Number online tools to reduce processing delays, minimize call volume, and improve response times.

- Improving the clarity of IRS tax forms and publications, including recommending updated guidance on Form 8821, Tax Information Authorization, regarding disclosure authority and revocation procedures.

Reinforcing the importance of in-person assistance to ensure taxpayers continue to have access to essential support services.

- Reducing wait times on IRS toll-free telephone lines by expanding secure chatbot and live chat capabilities to provide timely, personalized, and accessible customer service.

Tariffs: The Stickiness of Supply Networks; Tax Incidence vs. Tariff Refunds

The company that defied Trump’s tariff war - Sebastien Ash, Peter Foster and Alan Smith, Financial Times:

When the US president unveiled his “liberation day” tariffs in April 2025, the east German manufacturer — which sells industrial bolts and screws into the US — was facing a 20 per cent levy on its goods.

...

Schraubenwerk’s experience was in line with its peers, according to the FT’s analysis. Most of the world’s major exporters of screws and bolts to the US saw an approximately 10-fold increase in their effective tariff rate, but without any significant reduction in the overall volume of trade with America.

Which means, of course, increased costs to U.S. users of screws and bolts, with no benefit to US fastener makers.

Tariffs Raised Consumers’ Prices, but the Refunds Go Only to Businesses - Tony Romm, New York Times:

The discrepancy is a reflection of the nation’s complicated import laws — and the ever-fluid nature of Mr. Trump’s trade war.

...

For more than a year, Mr. Trump has insisted that foreigners, not Americans, have shouldered the financial burden of his punishing global trade war. But the data has always told a more complicated story, one in which Americans have actually been left to pay a substantial toll.

Economists understand that the person who writes the check for a tax isn't necessarily the person who bears the cost. That's true for tariffs, corporate taxes, and even "billionaire taxes."

High-end Taxes make California Ballot, Fail in Illinois

California’s Billionaire Tax Has the Signatures to Make the Ballot, Backers Say - Juliet Chung and Paul Kiernan, Wall Street Journal:

More than 1.5 million people have signed a petition to get the one-time, 5% wealth tax on statewide ballots in November, the people said. County election officials must tally the signatures, verify them, and send them to California’s secretary of state before the measure can appear on the ballot. The people familiar with the campaign said they expect that will be more than enough to clear the required 875,000-signature threshold, even after accounting for illegible or invalid signatures.

‘Millionaire tax’ proposal fails to advance in Illinois House - Jim Hagerty, Fox2Now:

House Speaker Emanuel “Chris” Welch, D-Hillside, confirmed Wednesday night that lawmakers would not call the amendment for a vote this week. The Illinois House is not scheduled to convene again before Thursday’s deadline to advance constitutional amendments for the November election.

The proposal, sponsored by Rep. La Shawn Ford, D-Chicago, would require voter approval to change Illinois’ constitution to allow higher taxes on income earned above $1 million. Illinois currently has a constitutionally mandated flat income tax.

Exempt Orgs Face New Form 990

IRS Will Revise Exempt Org Tax Form to Increase Transparency - Kelsey Brooks, Tax Notes ($):

Treasury says the changes to the form will reduce “fraud, abuse, and misuse of taxpayer dollars.” They follow heightened efforts to investigate suspected fraud in the nonprofit sector.

On February 13 Treasury announced that the IRS would launch a task force focused on investigating the misuse of funds by exempt organizations and that the department would be accepting whistleblower tips.

Related: Eide Bailly Exempt Organization Tax Services.

Blogs and Bits

AI’s potential to increase IRS audits raises expectations and fears - Kay Bell, Don't Mess With Taxes. "Last year, the IRS paid Palantir $1.8 million last year to improve a custom tool designed to help the tax agency identify the 'highest-value' cases for audits, collection of unpaid taxes, and potential criminal investigations, according to documents WIRED obtained via a public record request."

The Conservation Law of Tax Alpha - Samir Varma. "The math is clean, the academic papers are careful, and the more honest sponsor decks will say something like this in the footnotes. It is simply that the product is being sold as investing, and it largely works, to the extent it works, as estate planning with an investment wrapper."

Court Rejects Proposed Settlement Allowing Churches to Endorse Political Candidates - Parker Tax Pro Library. "A district court held that it did not have jurisdiction to enter a proposed consent judgment, agreed to by the IRS two churches and two other nonprofit groups focused on religious practice, that would have declared unconstitutional the provision in Code Sec. 501(c)(3) that bars exempt organizations from participating in political campaigns (i.e., the Johnson Amendment)."

Old Enough to Know Better

Connecticut CPA Sentenced to Prison for Tax Evasion - U.S. Attorney's Office, District of Connecticut (Defendant name omitted, emphasis added):

...From 2016 through 2022, Defendant prepared and filed annual joint income tax returns with the Internal Revenue Service on behalf of himself and his spouse. He also filed annual partnership income tax returns for an entity named FinGLTD, which he owned with his spouse. During this seven-year period, Defendant cashed more than 2,000 client payment checks to hide income generated by [his CPA practice]. As a result, a substantial amount of business receipts was diverted... and not reported in his joint income tax returns (Forms 1040 and 1040-SR) or partnership income tax returns (Form 1065).

Defendant deposited funds derived from the cashed checks, as well as client payment checks... into a network of business, personal, and nominee accounts. He maintained, controlled, and used 15 different bank accounts to deposit business receipts and to evade income taxes. Through this scheme, Defendant failed to report to the IRS $1,379,694.21 in additional income, resulting in a tax loss to the government of $422,720.

Defendant has paid the IRS $422,720, but still owes substantial interest and penalties.

Unfortunately for this hapless CPA, that much income leaves breadcrumbs behind that the IRS computers can notice. If a veteran CPA can't pull this off, it's unlikely the random business owner can. He could have saved a lot of effort (15 bank accounts!) just by paying the taxes in the first place.

What day is it?

It's Marine Mammal Rescue Day! Or at least take a manatee to lunch.