Key Takeaways

- IRS’s second year funding plan

- IRA Notice

- PIN requirement

- Debating tax fairness

- The coming TCJA squabble

- Incoming: PTEP guidance

- Making the call

- Getting It Done.

The Tax News & Views Roundup will be on hiatus after today until January 2nd. Happy New Year to all and may 2024 be a good one!

Funding Is Key to the IRS’s Big 2024 Enforcement, Service Agenda -Erin Slowey, Bloomberg ($):

The IRS, in its second full year with the infusion of billions in tax-and-climate law funds, is set to continue its 150-page plan for the money and flaunt to Congress just what a funded IRS can do.

Since it was provided the new funds, the Internal Revenue Service has started to revamp how it’s going after tax cheats and make it easier for taxpayers to manage what they owe.The recent IRS restructuring—the addition of four new top leadership roles and slim down to one deputy commissioner—further cements what the agency plans to prioritize in the coming year: taxpayer service, tax compliance, operations, and information technology.

A Look Ahead: Service Improvements and Enforcement Seen as IRS Funding Target – Lauren Loricchio, Tax Notes ($):

The IRS received nearly $80 billion in supplemental funding to spend through 2031 from the IRA, with $45.6 billion allocated for enforcement, $3.2 billion for taxpayer services, $25.3 billion for operations support, and $4.8 billion for business systems modernization. However, about $21.4 billion of the funding is set to be rolled back by congressional Republicans as part of a debt limit deal, with $1.4 billion immediately rescinded under the Fiscal Responsibility Act of 2023 (H.R. 3746).

An October report from the Treasury Inspector General for Tax Administration found that as of June 30, the IRS had spent about $1.95 billion, or 2.5 percent, of its IRA funding. Of that amount, $561.4 million has gone to taxpayer services, $93.7 million to enforcement, $850.5 million to operations support, and $431.6 million to business systems modernization funding, while no funds were directed to energy security.

The TIGTA report is here.

The Department of the Treasury and the Internal Revenue Service today issued Notice 2024-9 that provides procedures for applicable entities to claim the statutory exception to the application of the phaseouts for elective payment projects that begin construction during calendar year 2024 that fail to satisfy the domestic content requirement.

The phaseouts for elective payment and the statutory exception apply to the following credits:

- Renewable Electricity Production Credit (IRC § 45)

- Clean Electricity Production Credit (IRC § 45Y)

- Energy Credit (IRC § 48)

- Clean Electricity Investment Credit (IRC § 48E)

Guidance Proposed for Domestic Content Phaseouts Exceptions - Caleb Harshberger, Bloomberg ($):

Treasury and the IRS issued proposed guidance on exceptions to tax credit phaseouts for entities that don’t meet domestic content requirements, according to a notice (Notice 2024-9) released Thursday.

The guidance includes procedures for applicable entities to claim the exceptions to phaseouts for elective payment projects that fail to satisfy the domestic content requirement and that begin construction during 2024.

IRS Details Phaseout Exceptions for Domestic Content Requirements – Mary Katherine Browne – Tax Notes ($):

The phaseout exceptions allow a taxpayer to avoid credit phaseouts if it provides an attestation that it has reviewed the requirements for the increased cost exception and the nonavailability exception found in section 45(b)(10)(D) and has made a good-faith determination that it qualifies for either exception or both. The attestation must be attached to a Form 8835, “Renewable Electricity Product Credit,” a Form 3468, “Investment Credit,” or any other applicable form that can be filed to claim an elective payment under section 6417.

The Notice is here.

The Department of the Treasury and the Internal Revenue Service issued Notice 2024-13 announcing that the IRS intends to propose regulations to implement the product identification number (PIN) requirement with respect to the energy efficient home improvement credit…

Beginning on Jan. 1, 2025, taxpayers claiming the credit must also satisfy the PIN requirement for certain categories of products. Under this requirement, an item will only qualify for the energy efficient home improvement credit if the item is produced by a qualified manufacturer, and if the taxpayer includes the qualified PIN of the item on their tax return.

The Notice is here.

Tennessee twister victims get tax relief, including a new June 17, 2024, filing deadline – Kay Bell, Don’t Mess With Taxes:

On Dec. 9 and 10, at least six tornadoes touched down in Middle Tennessee.

The National Weather Service (NWS) said that the EF-3 tornado in the Clarksville's area carved a path 42 miles long with winds estimated at 150 miles per hour. Another tornado was an EF-2 that traveled 31 miles, leaving a path of damage in Nashville, Madison, Hendersonville, and Gallatin…

Following Federal Emergency Management Agency (FEMA) assessments that led the White House to declare parts of Tennessee as major disaster areas, the Internal Revenue Service granted the storm-affected residents tax relief.

The IRS document was released on December 22nd and is here.

IRS Addresses Basis Issue Tied to Previously Taxed Income - Michael Rapoport and Lauren Vella: Bloomberg ($):

The IRS issued a notice addressing basis adjustments that can result when a transaction pushes a foreign affiliate higher in a company’s structure.

The guidance 2024-16, issued Thursday, is related to but separate from the IRS’s broader forthcoming regulations addressing previously taxed earnings and profits, or PTEP. An IRS official said at a recent conference that the broader notice would be coming soon.

The guidance is here.

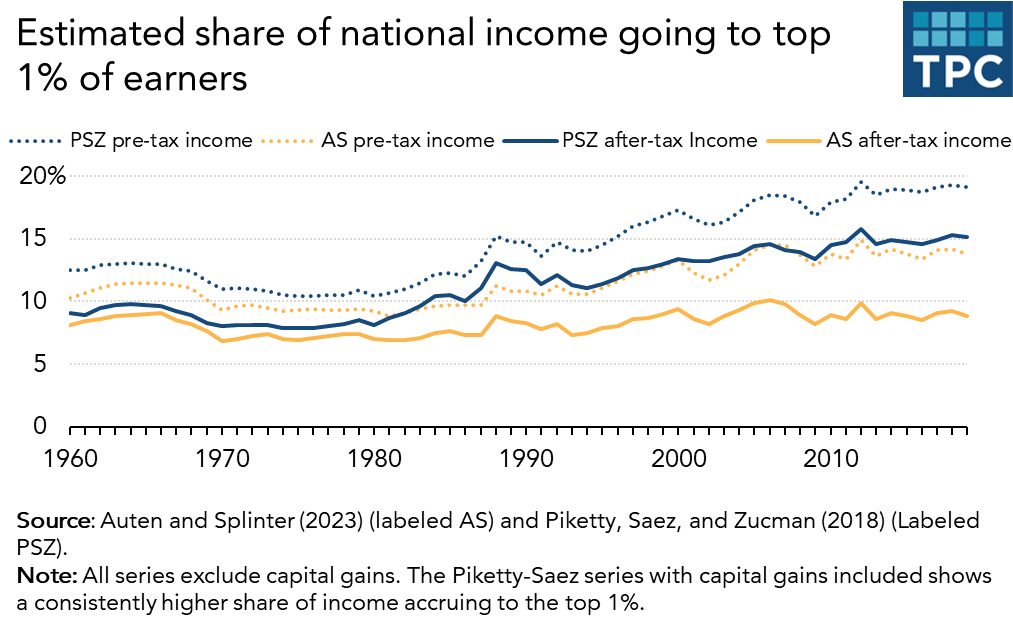

Measuring Income Inequality: A Primer On The Debate – William Gale, John Sabelhaus and Samuel Thorpe, Tax Policy Center:

There is substantial evidence that income inequality in America rose throughout the late 20th and early 21st centuries. Influential research by Thomas Piketty, Emmanuel Saez, and Gabriel Zucman (PSZ) finds that inequality has risen markedly, with the top 1% of taxpayers’ share of after-tax-and-transfer income rising from 9% in 1960 to 15% in 2019.

Recently published work by Gerald Auten and David Splinter (AS) paints a different picture. The authors find that inequality has barely budged, with the top 1% receiving 9% of after-tax income in 2019, up only slightly from 8% in 1960.

Remarkably, the two author teams use the same income concept (national income) and the same data (based on tax returns) to generate these contrasting results. How can such different conclusions arise given the similarity in approach? And what is the right way to characterize income inequality?

Income inequality (or equality) will be a huge topic in 2024 as lawmakers next year are expected to debate which of the expiring tax provisions in the Tax Cuts and Jobs Act should be extended beyond 2025.

And the outcome of the 2024 elections will have a huge impact on tax policy.

A Look Ahead: Showdown Looms for Competing Tax Policy Visions – Alexander Rifaat, Tax Notes ($):

While issues such as abortion, immigration, and the war in Ukraine are sure to dominate the political ecosystem in the coming year, there’s one inconvenient subject that might need to make its way onto the campaign trail.

“The elephant in the room that maybe no one is going to want to talk about, but they’re going to have to, is that huge parts of the [Tax Cuts and Jobs Act] are scheduled to expire in 2025. One way or the other, whoever wins the presidency is going to have to deal with them,” noted Marc Goldwein of the Committee for a Responsible Federal Budget.

IRS to Issue Proposed Regs Addressing PTEP Basis Treatment – Kiarra Strocko, Tax Notes ($):

Treasury and the IRS plan to issue additional proposed regulations related to previously taxed earnings and profits (PTEP) that will address basis consequences of a liquidation or an asset reorganization of top-tier controlled foreign corporations.

Notice 2024-16, published December 28, says that these additional proposed regs related to basis adjustments in stock held by a foreign corporation are separate from the long-awaited PTEP proposed regs, which are expected to be released in the the first half of 2024. The PTEP proposed regs were originally slated for release in 2019, but the release date has been pushed back several times. Treasury has indicated that guidance will be released in tranches given its complexity.

The Notice is here.

Scoop: Biden in "frustrating" call told Bibi to solve Palestinian tax revenue issue - Barak Ravid, Axios:

President Biden held a difficult conversation last weekend with Israeli Prime Minister Benjamin Netanyahu over Israel's decision to withhold part of the tax revenue it collects for the Palestinian Authority, according to two U.S. and Israeli officials and a source with knowledge of the issue…

Catch up quick: The tax revenues Israel collects for the Palestinian Authority under an agreement between the parties are a major source of income for the PA, which is already in a financial crisis.

From the “Know Your Stuff” file:

You make the call - NATP Research, National Association of Tax Professionals:

Question: Pepé is a casual gambler and went to the casino several times throughout the year. His total gambling winnings for the year are $3,500. On the advice of his accountant, he kept a detailed log of all the transactions related to his gambling. At the end of the year, he determined that he had $5,000 in gambling losses. Can Pepé use his gambling losses to directly offset his gambling winnings and report a net gambling gain of $0 on his tax return?

Answer: No. Pepé cannot net his gambling winnings and losses. Instead, he must report all his gambling winnings as income on his Form 1040, U.S. Individual Income Tax Return, using Schedule 1, Additional Income and Adjustments to Income, Line 8b.

He may then deduct the losses to the extent of the gambling winnings as a miscellaneous itemized deduction not subject to the 2% AGI limitation on Schedule A, Itemized Deductions, using Line 16.

Happy No Interruptions Day! The last work day before the new year is a great time to clear the decks:

- Answer un-answered emails

- Delete, file, and organize emails we've been saving

- Scan needed receipts and shred unnecessary paperwork

- Complete online training courses

- Update calendar and address book.

Also, Happy New Year!