IRS Gears Up Fax Machines for Specified Quick Refund Claims - Emily Foster and Andrew Velarde, Tax Notes. "Taxpayers may soon be able to fax requests for quick refund claims for alternative minimum tax credits and net operating loss deductions that previously could only be filed via hard copy though mail delivery services."

Yes, the venerable fax machine, like a 1960s-era programming language, still plays a key role in administering the tax system.

The IRS last week allowed taxpayers with Net Operating losses to use streamlined filings - Form 1045 for individuals, Form 1139 for Corporations - to claim 2018 net operating loss carrybacks, provided the Forms are filed by June 30, 2020. Unfortunately, the IRS has no ability to process such claims electronically. Unless faxes count. From an IRS release issued yesterday:

Starting on April 17, 2020 and until further notice, the IRS will accept eligible refund claims Form 1139 submitted via Fax to 844-249-6236 and eligible refund claims Form 1045 submitted via fax to 844-249-6237. Before then, these fax numbers will not be operational. We encourage taxpayers to wait until this procedure is available rather than mail their Forms 1139 and 1045 since mail processing is being impacted by the emergency.

So dust off your 10-key, do your supporting schedules on some 14-column ledger paper, and get those faxes in starting Friday.

IRS Allows Faxed Tax Refund Claims, Here’s How - Robert Woods, Forbes. "A maximum of 100 pages can be initially faxed."

Reversed Elections, Amended Returns, And NOL Carrybacks: The IRS Provides Guidance On CARES Act Tax Changes - Tony Nitti, Forbes. "June 30 is approaching rapidly, so get those Forms 1139 and 1045 for 2018 NOLs going posthaste."

State tax deadlines mostly July 15, too - Kay Bell, Don't Mess With Taxes. "Some states, for example, have extended annual return filing and paying, but have not extended the deadline for filing estimated taxes due on April 15. Yes, that's this week. Just a couple of days from now."

Hesitancy to Use Workarounds Could Imperil State Efforts to Beat SALT Cap - Lauren Loricchio, Tax Notes ($). The article addresses provisions enacted in some states for passthrough entities to choose to be taxed at the entity level. Entity-level taxes are understood to be fully deductible, while individual income taxes are subject to a $10,000 overall cap on deductions for state and local taxes. But, according to this article, passthrough entities are not rushing to be taxed.

Louisiana is one such state:

Jared Walczak of the Tax Foundation said the taxpayer benefits of the Louisiana workaround are limited and “may well be more than offset by the disadvantages of operating under a corporate income tax structure.”

Louisiana allows passthrough businesses to elect to be taxed as C corporations under an alternative corporate income tax rate structure to allow their owners to avoid the SALT deduction cap, Walczak explained.

Congressional efforts are underway to remove the $10,000 cap as part of the next round of COVID-19 legislation, but prospects are uncertain.

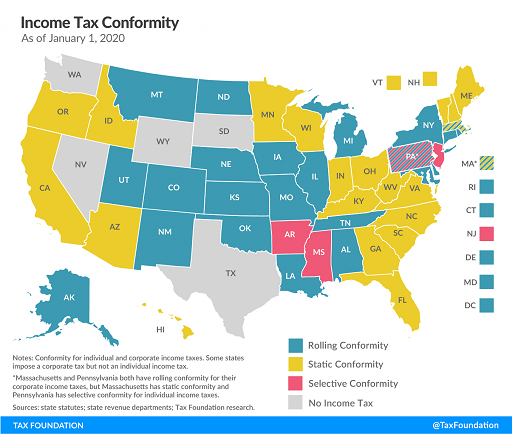

Will States Tax the Federal Government’s COVID-19 Lifeline to Small Businesses? - Jared Walczak, Tax Policy Blog. "States with what is known as rolling conformity are set; they will not tax the forgiveness of federal loans under the PPP unless lawmakers in those states adopt a law expressly doing so. But with static conformity states, it all depends on if and when they update their conformity."

Starting in 2020, Iowa automatically conforms to federal rules. States that will have to pass legislation to conform to federal treament include Arizona, California, Idaho and Minnesota.

How Will I Get My CARES Stimulus Payment if my Preparer Paid My Refund? - Connor Moran, Procedurally Taxing. Why refund anticipation loans gum up the COVID-19 tax rebates:

This issue generally arises when a low income taxpayer goes to a paid preparer and lacks the money to pay the preparer for the cost of preparation and/or wants the refund immediately rather than waiting for the IRS to deposit the refund in their bank account, if the taxpayer has one, or receipt of a paper check. Rather than pay up front for tax preparation services, the taxpayer agrees to let the preparer set up a temporary bank account into which the IRS will deposit the tax refund. Tax preparer fees are deducted straight from the refund, and the preparer either gives the taxpayer a check up front or a prepaid debit card that will be funded when the refund arrives.

See the problem?

If you used one of these services, the IRS doesn’t have your bank account information, but it maybe thinks that it does.

Not even giving away money is simple.

Looking To Update Direct Deposit Or Get More Info From IRS About Your Stimulus Check? Kelly Phillips Erb, Forbes:

To clarify, the IRS is building a second tool. That tool, Get My Payment, is expected to be available by April 17. It will:

- Provide you with the status of your payment, including the date your payment is scheduled to be deposited into your bank account or mailed; and

- Allow eligible taxpayers a chance to provide bank account information to receive payments more quickly rather than waiting for a paper check. This feature will be unavailable if the Economic Impact Payment has already been scheduled for delivery.

IRS: “Don’t Call Us. Don’t Expect Us to Read Your Mail for a While.” - Russ Fox, Taxable Talk. "All IRS phone lines have been shut down. The IRS CAF unit is shut down, so tax professionals can’t send Powers of Attorney or Tax Information Authorizations. Mail is not being picked up by the IRS."

Tax returns are being processed, to be sure, but not much else.

Who Should Pay For The Economic Relief From The COVID-19 Crisis? - Eugene Steuerle, TaxVox. "Simply as a matter of fairness, delay on specifying the payment mechanisms weakens the message that 'we’re all in this together.'"

Income Tax-Related Provisions of Emergency Relief Legislation - Roger McEowen, Agricultural Law and Taxation Blog. "The legislation allows corporations to claim 100 percent of AMT credits in 2019 as fully refundable and provides an election to accelerate claims to 2018, with eligibility for accelerated refunds."

Economic Analysis: Self-Employed Loan Forgiveness Uncertain, Illogical, Pliable - Martin Sullivan, Tax Notes. "To the extent one policy goal of the CARES Act is to provide relief to those most in need, this result does the opposite of what is intended: Relatively healthy businesses gets significant forgiveness, and distressed businesses get no forgiveness."

Technology changes, but bad tax ideas are timeless. A New York Times obituary reminds us that before there was a Reddit, there was Usenet, and before there was r/tax, there was misc.taxes.moderated.

The obituary is for a man who started out running "small-time investment and marketing scams in Topeka" but who rose to improbable prominence in the tax world in the early days of the Internet:

He launched Renaissance/The Tax People, a tax-avoidance business that ultimately ensnared about 50,000 Americans — until a Kansas state judge shut the firm down in 2001, ruling that it was an illegal pyramid scheme of a “fundamentally deceptive nature” that had cost customers and investors at least $84 million.

Some of my first experience with this new "Internet" thing was wandering into misc.tax.moderated (it's still there!) to read the astonishing claims made for the "Dream Team" of Renaissance/The Tax People. The obituary, for a Mr. Cooper, gives some of the flavor:

In an interview in his San Diego hotel suite in 2000, Mr. Cooper told a reporter that dropping a business card in a fishbowl at a restaurant’s cash register made the meal, parking and mileage to and from the establishment tax-deductible. Asked by The Times to identify a statute, regulation or court case authorizing such deductions, Mr. Cooper said the answer was in his company’s promotional materials. Advised that no authority was cited in those materials, Mr. Cooper said the right to such deductions was common knowledge. He then said that one of his “Tax Dream Team” experts would explain. When asked which team member should be queried, Mr. Cooper stood up and walked out of the room.

In misc.taxes.moderated, nobody ever seemed to leave the room, though I eventually did, discovering and joining the early tax blogs.

Mr. Cooper died in federal prison before he could complete a 25-year sentence arising out of his tax advice. We can assume his clients had a heavy examination rate and many return adjustments. The lesson he leaves behind lives: there is always somebody with a patina of authority - a "tax dream team," if you will - willing to give the tax answer you really want when the answer your tax advisor gives you is unpleasant. There will always be somebody who says your current tax advisor is too conservative, behind the times, acts like an IRS agent, whatever. Heeding that somebody can be very expensive.